ℹ️ Skipped - page is already crawled

| Filter | Status | Condition | Details |

|---|---|---|---|

| HTTP status | PASS | download_http_code = 200 | HTTP 200 |

| Age cutoff | PASS | download_stamp > now() - 6 MONTH | 0.5 months ago |

| History drop | PASS | isNull(history_drop_reason) | No drop reason |

| Spam/ban | PASS | fh_dont_index != 1 AND ml_spam_score = 0 | ml_spam_score=0 |

| Canonical | PASS | meta_canonical IS NULL OR = '' OR = src_unparsed | Not set |

| Property | Value | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| URL | https://www.guideline.com/education/articles/how-much-should-i-contribute-to-my-401-k | |||||||||

| Last Crawled | 2026-04-08 19:19:35 (16 days ago) | |||||||||

| First Indexed | 2024-08-09 16:49:48 (1 year ago) | |||||||||

| HTTP Status Code | 200 | |||||||||

| Content | ||||||||||

| Meta Title | 401(k) Contribution Limits in 2024 | Guideline | |||||||||

| Meta Description | Learn how you can maximize your retirement savings this year with this 2024 401(k) contribution overview. | |||||||||

| Meta Canonical | null | |||||||||

| Boilerpipe Text | When it comes to the question of how much you should contribute to your 401(k) account, there’s no right or wrong answer. At Guideline, our goal is to provide everyone with a path to retirement, and what that path looks like could change based on your personal goals and circumstances.

And whether you’re just getting started with a 401(k) for the first time or you’re a bit farther along in your journey, it’s never too late or too early to learn more about saving for retirement. As with any financial decision, consulting with an advisor or tax professional can help determine what's best for you.

Let’s talk about your 401(k)

.

Keep reading to learn more about:

Maximum allowable contributions

Employer match

Factors to help you determine what might be the right amount for you

Know your limits

The IRS — not your employer or your retirement account brokerage — sets the maximum amount an individual may contribute to their 401(k) each year. As we covered in

this article

, there are tax advantages to contributing to a 401(k) and these contribution limits are put in place by the IRS to ensure those tax advantages are enjoyed fairly by everyone.

What is the maximum amount I can contribute to my 401(k) each year?

Known as the 402(g) limit in the Internal Revenue Code (or IRC), individuals can contribute up to $24,500 between their traditional and Roth 401(k) accounts in 2026. If you’re 50 or older, you can contribute an additional $8,000 ($32,500 in total) thanks to what’s known as a catch-up contribution.

1

And beginning in 2025, there is now an extended catch-up allowing individuals aged 60-63 to contribute $11,250 (for a total of $35,750 in 2026).

1

While these limits may stay the same some years, they are re-evaluated by the IRS every year to consider cost-of-living adjustments and are subject to change annually.

Does that limit include what my employer contributes as well?

It’s important to note that these limits only account for what you as an individual saver are contributing to your account, not the amount an employer may be contributing on your behalf. The total amount that can be contributed to your 401(k), also known as the 415(c) limit, inclusive of both your own paycheck deferrals and any employer contributions, is $72,000 in 2026. That limit increases to $80,000 if you are 50 or older (and $83,250 if you’re 60-63 and eligible for the extended catchup). The IRS also stipulates that your 401(k) contributions may not exceed 100% of your taxable income.

The 415(c) limit is reevaluated and typically increases alongside the 402(g) limit annually.

If I have access to more than one 401(k) in a single year, does that change how much I can contribute?

Since the deferral limits are individual limits, they apply to all of your contributions in a given tax year. Therefore, if you switch jobs halfway through the year, your deferral limit does not reset.

It’s important to tell a new provider of any 401(k) contributions you might have made to date when enrolling to avoid over-contributing by accident. More on this below.

Let’s review these limits with two examples:

In 2026, a 39-year-old is employed by two companies, both of which offer a 401(k) benefit: Company A from January through September and Company B from October through December. They’ve already contributed $10,000 to their 401(k) with Company A. Therefore, when enrolling with Company B’s 401(k) provider, it’s important to remember that the limit does not reset and that they cannot exceed the $24,500 limit. One way to avoid over-contributing is making sure to inform Company B’s 401(k) provider of the $10,000 already contributed that year.

Now, a 53-year-old is employed full time by two companies in the same year, both of which offer a 401(k) benefit. In addition to their full-time jobs, they have been hired in a part-time seasonal role for the holidays, and that company offers a 401(k) to their part-time employees. This individual saver is already tracking towards contributing $24,500 to their 401(k) between Company A and Company B. Therefore, when enrolling with Company C’s 401(k) provider, any additional contributions cannot exceed $8,000 (based on the IRS’ contribution limits with catch-up contributions for 2026).

Do rolled over funds count towards my contribution limit?

It depends. If you made the contribution in the same tax year, then the amount you contributed will count towards your contribution limit, regardless if you rolled them over. If you have rolled over funds from a previous 401(k), but made the contribution in a previous tax year, that balance does not count towards your annual limit.

For example, let’s say you were employed at Company X over the course of two calendar years from April 2024 to April 2025, and then you joined Company Y in May 2025. Any contributions you made from April 2024 until December 31, 2024 would not count towards your 2025 limit, even if you roll it over to your Company Y 401(k) in 2025 (or any year thereafter).

1

What happens if I contribute above the IRS-allowable amount?

You could end up being taxed twice. Given the tax savings 401(k)s offer, the

IRS has consequences

, in the form of taxes, when plan participants exceed the allowable limit. While this may happen for a few reasons, a common reason is for not informing a second 401(k) provider of any contributions already made (or planned to make) in that tax year.

Guideline monitors your activity throughout the year and will notify you if you do exceed your limit for deferrals we are aware of. You can learn more about the process

here

.

Meeting your match

You may have heard this before, and no, we’re not talking about your other half.

What is a match and how can I meet it?

Depending on your employer’s 401(k) benefit, you may have access to what’s known as an ‘employer match’. It’s more or less what it sounds like - the employer will match your own contributions (also known as deferrals, since you’re deferring an amount from your salary) up to a certain amount.

This can take a few different forms, so it’s important to pay attention to what is required in order to earn the full amount of the match in your plan. Common examples of an employer match are:

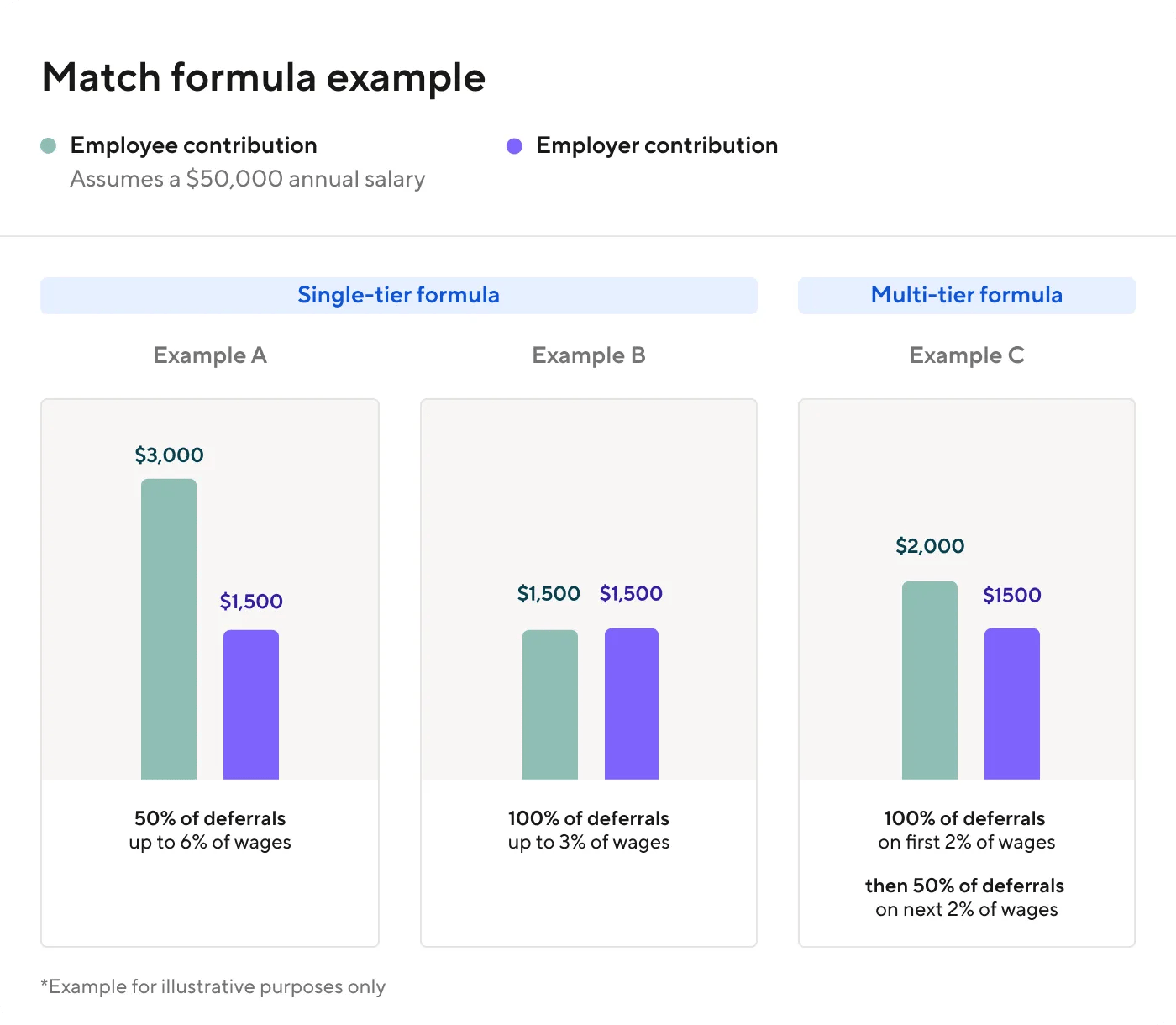

Single-tier formula:

The employer matches the same amount for each dollar that you contribute, up to a certain percentage of your income.

Example A: Your employer matches 50% of the first 6% of your contributions. In this case, you need to contribute at least 6% per-pay-period to earn your full match. Here, the employer is matching $.50 for each $1, up to 6% of your income.

Example B: Your employer matches 100% of the first 3% of your contributions. Therefore, you need to contribute at least 3% per-pay-period to earn your full match. Here, the employer is matching $1 for each $1 up to 3% of your income.

In both cases, the employer’s match is 3% of the employee’s income, but in the first example you would need to defer at least 6% to get the full 3% match.

Multi-tier formula:

The employer’s match may have different tiers, where the first tier is matched at one

ratio and subsequent tiers may be matched at different ratios

.

Example C: Your employer matches 100% on the first 2% and 50% on the next 2%. Therefore, you need to contribute at least 4% in order to earn the full match of 3%. Here, the employer is matching $1 for $1 on the first 2% contributed, and $.50 for each $1 contributed on the next 2%. In this example too, the employer’s match is 3% of the employee's income but you would need to defer at least 4% to get the full 3% match.

In both the single-tier and multi-tier formulas, any contributions made beyond what is required to earn the employer’s match, will not result in a higher match.

Why is it important to meet the match?

It can be helpful to think of your employer’s contribution to your 401(k) as part of your total salary. Therefore, if offered a match, it may be important to consider doing what you can to contribute the minimum amount required to earn your employer’s full match. By not meeting your match, you are effectively leaving money on the table and not earning your full wages. If we take a look back at the examples above - if one’s income is $50,000, by not contributing enough to meet their match, they could be leaving up to $1,500 of employer contributions to their retirement behind.

Can I contribute more than my match?

You can absolutely contribute more than your match, and it’s a great way to save more towards retirement while taking advantage of those tax-advantages. Do note that anything you contribute beyond what your employer matches will not earn any additional match.

Is the matched amount mine to take with me if I leave my employer?

It depends on your employer’s plan. Some employers may opt to include a vesting requirement, which may delay when you will have full access to your employer’s match. Just like the match formula can vary from plan to plan, so can the vesting schedule.

There are three types of vesting schedules:

Immediate vesting

: In this case, there is no term of employment required to earn your employer’s match.

Cliff vesting

:

After a predetermined amount of time, you unlock the full amount of your employer's match. For example, iIf you have a 2-year cliff, you unlock the full amount of your employer’s match after your 2 year anniversary with the company.

Graded vesting

:

There’s a bit more flexibility on the employer’s part here and can differ by plan. Generally, you gradually unlock a portion each year you are employed by your employer. It’s always good to familiarize yourself with your plan’s vesting schedule. Using the same 2-years as an example, if you have a 2-year graded vesting with equal vesting each year, you unlock the 50% of your employer’s match after your 1st year with the company, and 100% of your match after 2 years with the company.

Know that if your 401(k) plan has a vesting requirement and your match has not fully vested before you part ways with your employer, it only impacts the employer’s match, not what you contributed. Whatever you as the employee contributed to your account - including gains and losses - is yours to take with you as you continue on, regardless of vesting.

Finding your ‘just right’

Personal finances are just that - personal. There is not a single ‘right’ amount that everybody should be contributing to their retirement savings. There are, however, questions to help you in determining what might be the right amount for you.

1. Are you meeting your match?

We’ve said it before, and we’ll say it again. When evaluating your finances, it can be important to consider contributing the minimum amount required by your employer's plan to earn the full match. Not doing so is equivalent to not earning your full salary. While this may reduce your take-home pay, consider the growth potential of your retirement account from compound returns over the long run.

2. Are you able to contribute more than your match?

Maybe maxing out is not right for you but you feel comfortable contributing more than what’s required to earn your match. As we discussed earlier in this article, there is also not a single formula for determining an employer’s match, and therefore it may be possible for you to budget in a higher contribution amount (within the annual limits of course). To that we say “go forth and contribute”.

While you may not get more from your employer once you exceed your matching requirement, contributing more than your match allows you to not only save more, but also take greater advantage of your tax-advantaged account and compounding returns. That small change today may not feel like much, but could create a ripple effect come time for retirement.

We know that life happens and unexpected expenses come up. Know that you can

change your contribution amount at any time

- that goes for both increasing and decreasing.

When determining how much more you could possibly contribute towards your 401(k), it may be helpful to:

Examine your expenses:

Add up your average monthly expenses like rent or mortgage, utilities, food and entertainment. Make sure to include any student loans or credit card debt you’re paying down.

Chart your goals:

It may be helpful to consider retirement alongside a series of other milestones (like buying a home, raising children, going on vacations) and even unplanned expenditures (like medical bills) that have meaningful financial commitments on your path to retirement.

As we covered in this

article

, determine your risk tolerance and time to your goals as you consider saving for short and long term goals.

While a volatile market might be cause for concern, continued and consistent contributions allow you to invest via

dollar-cost averaging

, helping you to, in theory, reduce the overall impact that market volatility has on the price you pay to acquire more shares of your investments.

Explore your options:

Just like retirement should be considered alongside other short and long term goals, retirement savings accounts can be considered to be one part of your broader financial portfolio. Exploring other savings and investing options that fit your needs and adjusting as needed as your plans evolve can be effective. Moreover, take some time to learn more about other factors that can impact and help you on your broader financial journey:

Overall risk tolerance

Investment objective

Overall financial situation

Outside investment and retirement accounts

Prior investment experience

Tax bracket

Time horizon

3. Are you maxing out on your 401(k) contributions?

First things first — if you have a match, maxing out too early in the year can lead to missing out on a portion of your employer’s match. Once you max out and are no longer able to contribute for that tax year, your employer’s match will stop as well. In your Guideline account’s

contribution setting page

, we’ll alert you if the amount you’ve elected to contribute will push you into this territory so you can adjust your deferral amount and get the most value from your Guideline 401(k) each year.

Now, if you are already contributing the maximum allowable amount to your 401(k) ($24,500 in 2026, $32,500 if you are 50+, and $35,750 if you’re 60-63) and looking to save more with a dedicated retirement account, consider contributing to an

IRA

.

1

IRAs offer similar advantages to a 401(k) and allow you to contribute an additional $7,500 ($8,600 if 50+) in 2026. In addition to this uppermost limit, there are contribution limits and considerations based on your income, which are covered

here

.

Takeaways:

Meet your match

: By not contributing the minimum amount required to meet your match, you are effectively leaving money on the table. While it may not seem consequential today, when you consider the effect of

compound returns

, a few percentage points today can in theory grow into a meaningful sum by the time you retire.

Optimize your max

: If you have an employer match, don’t max out too early in the year, as you may leave some of your match on the table.

Don’t exceed the max

: Be mindful of the annual contribution limit, especially if you have access to more than one 401(k) account in a single tax year. Over-contributing requires you to return the excess amount in due time to avoid paying taxes twice and avoid a 10% penalty. Depending on when this takes place, you may need to request a new W2 to ensure your taxable income is correct on your tax return. You can learn more about the process

here.

Strike the right balance

: Finances are an incredibly personal topic. Consider your bigger picture — as detailed or as broad as you're comfortable with — and what other financial commitments you may have up ahead. You can change your contribution amount at any time. So, if you’ve decided to contribute 10% but you have an unexpected financial expense and need to scale back for a few months (but not below your match of course), that’s certainly allowable.

Give your employees a roadmap to retirement

With Guideline, you can provide an impactful work benefit while minimizing paperwork and fees. | |||||||||

| Markdown | [](https://www.guideline.com/)

[What we offer](https://www.guideline.com/what-we-offer?gl_cta=navbar)[Education](https://www.guideline.com/education?gl_cta=navbar)[Pricing](https://www.guideline.com/pricing?gl_cta=navbar)

[What we offer](https://www.guideline.com/what-we-offer?gl_cta=navbar)

[Education](https://www.guideline.com/education?gl_cta=navbar)

[Pricing](https://www.guideline.com/pricing?gl_cta=navbar)

[Log in](https://my.guideline.com/login?gl_cta=navbar)[Get started](https://www.guideline.com/get-started?gl_cta=navbar&returnUrl=https%3A%2F%2Fwww.guideline.com%2Feducation%2Farticles%2Fhow-much-should-i-contribute-to-my-401-k&source=%2Feducation%2Farticles%2Fhow-much-should-i-contribute-to-my-401-k&token=schedule-demo)

[Log in](https://my.guideline.com/login?gl_cta=navbar)[Get started](https://www.guideline.com/get-started?gl_cta=navbar&returnUrl=https%3A%2F%2Fwww.guideline.com%2Feducation%2Farticles%2Fhow-much-should-i-contribute-to-my-401-k&source=%2Feducation%2Farticles%2Fhow-much-should-i-contribute-to-my-401-k&token=schedule-demo)

[Log in](https://my.guideline.com/login?gl_cta=navbar)

[Savers](https://www.guideline.com/education/audiences/savers)

**•**14 min read**•**

March 13, 2025

# How much should I contribute to my 401(k)?

Guideline Team

When it comes to the question of how much you should contribute to your 401(k) account, there’s no right or wrong answer. At Guideline, our goal is to provide everyone with a path to retirement, and what that path looks like could change based on your personal goals and circumstances.

And whether you’re just getting started with a 401(k) for the first time or you’re a bit farther along in your journey, it’s never too late or too early to learn more about saving for retirement. As with any financial decision, consulting with an advisor or tax professional can help determine what's best for you.

Let’s talk about your 401(k)**.** Keep reading to learn more about:

- Maximum allowable contributions

- Employer match

- Factors to help you determine what might be the right amount for you

## Know your limits

The IRS — not your employer or your retirement account brokerage — sets the maximum amount an individual may contribute to their 401(k) each year. As we covered in [this article](https://www.guideline.com/education/articles/difference-between-traditional-and-roth-401k), there are tax advantages to contributing to a 401(k) and these contribution limits are put in place by the IRS to ensure those tax advantages are enjoyed fairly by everyone.

### What is the maximum amount I can contribute to my 401(k) each year?

Known as the 402(g) limit in the Internal Revenue Code (or IRC), individuals can contribute up to \$24,500 between their traditional and Roth 401(k) accounts in 2026. If you’re 50 or older, you can contribute an additional \$8,000 (\$32,500 in total) thanks to what’s known as a catch-up contribution.1 And beginning in 2025, there is now an extended catch-up allowing individuals aged 60-63 to contribute \$11,250 (for a total of \$35,750 in 2026).1

While these limits may stay the same some years, they are re-evaluated by the IRS every year to consider cost-of-living adjustments and are subject to change annually.

### Does that limit include what my employer contributes as well?

It’s important to note that these limits only account for what you as an individual saver are contributing to your account, not the amount an employer may be contributing on your behalf. The total amount that can be contributed to your 401(k), also known as the 415(c) limit, inclusive of both your own paycheck deferrals and any employer contributions, is \$72,000 in 2026. That limit increases to \$80,000 if you are 50 or older (and \$83,250 if you’re 60-63 and eligible for the extended catchup). The IRS also stipulates that your 401(k) contributions may not exceed 100% of your taxable income.

The 415(c) limit is reevaluated and typically increases alongside the 402(g) limit annually.

### If I have access to more than one 401(k) in a single year, does that change how much I can contribute?

Since the deferral limits are individual limits, they apply to all of your contributions in a given tax year. Therefore, if you switch jobs halfway through the year, your deferral limit does not reset.

It’s important to tell a new provider of any 401(k) contributions you might have made to date when enrolling to avoid over-contributing by accident. More on this below.

Let’s review these limits with two examples:

- In 2026, a 39-year-old is employed by two companies, both of which offer a 401(k) benefit: Company A from January through September and Company B from October through December. They’ve already contributed \$10,000 to their 401(k) with Company A. Therefore, when enrolling with Company B’s 401(k) provider, it’s important to remember that the limit does not reset and that they cannot exceed the \$24,500 limit. One way to avoid over-contributing is making sure to inform Company B’s 401(k) provider of the \$10,000 already contributed that year.

- Now, a 53-year-old is employed full time by two companies in the same year, both of which offer a 401(k) benefit. In addition to their full-time jobs, they have been hired in a part-time seasonal role for the holidays, and that company offers a 401(k) to their part-time employees. This individual saver is already tracking towards contributing \$24,500 to their 401(k) between Company A and Company B. Therefore, when enrolling with Company C’s 401(k) provider, any additional contributions cannot exceed \$8,000 (based on the IRS’ contribution limits with catch-up contributions for 2026).

### Do rolled over funds count towards my contribution limit?

It depends. If you made the contribution in the same tax year, then the amount you contributed will count towards your contribution limit, regardless if you rolled them over. If you have rolled over funds from a previous 401(k), but made the contribution in a previous tax year, that balance does not count towards your annual limit.

For example, let’s say you were employed at Company X over the course of two calendar years from April 2024 to April 2025, and then you joined Company Y in May 2025. Any contributions you made from April 2024 until December 31, 2024 would not count towards your 2025 limit, even if you roll it over to your Company Y 401(k) in 2025 (or any year thereafter).1

### What happens if I contribute above the IRS-allowable amount?

You could end up being taxed twice. Given the tax savings 401(k)s offer, the [IRS has consequences](https://www.irs.gov/retirement-plans/consequences-to-a-participant-who-makes-excess-deferrals-to-a-401k-plan?ref=guideline.com), in the form of taxes, when plan participants exceed the allowable limit. While this may happen for a few reasons, a common reason is for not informing a second 401(k) provider of any contributions already made (or planned to make) in that tax year.

Guideline monitors your activity throughout the year and will notify you if you do exceed your limit for deferrals we are aware of. You can learn more about the process [here](https://help.guideline.com/en/articles/8605068-what-happens-if-i-overcontribute-to-my-401-k-account).

## Meeting your match

You may have heard this before, and no, we’re not talking about your other half.

### What is a match and how can I meet it?

Depending on your employer’s 401(k) benefit, you may have access to what’s known as an ‘employer match’. It’s more or less what it sounds like - the employer will match your own contributions (also known as deferrals, since you’re deferring an amount from your salary) up to a certain amount.

This can take a few different forms, so it’s important to pay attention to what is required in order to earn the full amount of the match in your plan. Common examples of an employer match are:

**Single-tier formula:** The employer matches the same amount for each dollar that you contribute, up to a certain percentage of your income.

Example A: Your employer matches 50% of the first 6% of your contributions. In this case, you need to contribute at least 6% per-pay-period to earn your full match. Here, the employer is matching \$.50 for each \$1, up to 6% of your income.

Example B: Your employer matches 100% of the first 3% of your contributions. Therefore, you need to contribute at least 3% per-pay-period to earn your full match. Here, the employer is matching \$1 for each \$1 up to 3% of your income.

In both cases, the employer’s match is 3% of the employee’s income, but in the first example you would need to defer at least 6% to get the full 3% match.

**Multi-tier formula:** The employer’s match may have different tiers, where the first tier is matched at one [ratio and subsequent tiers may be matched at different ratios](https://www.guideline.com/education/articles/understanding-401-k-expense-ratios-and-why-they-matter).

Example C: Your employer matches 100% on the first 2% and 50% on the next 2%. Therefore, you need to contribute at least 4% in order to earn the full match of 3%. Here, the employer is matching \$1 for \$1 on the first 2% contributed, and \$.50 for each \$1 contributed on the next 2%. In this example too, the employer’s match is 3% of the employee's income but you would need to defer at least 4% to get the full 3% match.

In both the single-tier and multi-tier formulas, any contributions made beyond what is required to earn the employer’s match, will not result in a higher match.

### Why is it important to meet the match?

It can be helpful to think of your employer’s contribution to your 401(k) as part of your total salary. Therefore, if offered a match, it may be important to consider doing what you can to contribute the minimum amount required to earn your employer’s full match. By not meeting your match, you are effectively leaving money on the table and not earning your full wages. If we take a look back at the examples above - if one’s income is \$50,000, by not contributing enough to meet their match, they could be leaving up to \$1,500 of employer contributions to their retirement behind.

### Can I contribute more than my match?

You can absolutely contribute more than your match, and it’s a great way to save more towards retirement while taking advantage of those tax-advantages. Do note that anything you contribute beyond what your employer matches will not earn any additional match.

### Is the matched amount mine to take with me if I leave my employer?

It depends on your employer’s plan. Some employers may opt to include a vesting requirement, which may delay when you will have full access to your employer’s match. Just like the match formula can vary from plan to plan, so can the vesting schedule.

There are three types of vesting schedules:

- **Immediate vesting**: In this case, there is no term of employment required to earn your employer’s match.

- [**Cliff vesting**](https://help.guideline.com/en/articles/8593684-what-is-a-cliff-vesting-schedule)**:** After a predetermined amount of time, you unlock the full amount of your employer's match. For example, iIf you have a 2-year cliff, you unlock the full amount of your employer’s match after your 2 year anniversary with the company.

- [**Graded vesting**](https://help.guideline.com/en/articles/8593694-what-is-a-graded-vesting-schedule)**:** There’s a bit more flexibility on the employer’s part here and can differ by plan. Generally, you gradually unlock a portion each year you are employed by your employer. It’s always good to familiarize yourself with your plan’s vesting schedule. Using the same 2-years as an example, if you have a 2-year graded vesting with equal vesting each year, you unlock the 50% of your employer’s match after your 1st year with the company, and 100% of your match after 2 years with the company.

Know that if your 401(k) plan has a vesting requirement and your match has not fully vested before you part ways with your employer, it only impacts the employer’s match, not what you contributed. Whatever you as the employee contributed to your account - including gains and losses - is yours to take with you as you continue on, regardless of vesting.

## Finding your ‘just right’

Personal finances are just that - personal. There is not a single ‘right’ amount that everybody should be contributing to their retirement savings. There are, however, questions to help you in determining what might be the right amount for you.

### 1\. Are you meeting your match?

We’ve said it before, and we’ll say it again. When evaluating your finances, it can be important to consider contributing the minimum amount required by your employer's plan to earn the full match. Not doing so is equivalent to not earning your full salary. While this may reduce your take-home pay, consider the growth potential of your retirement account from compound returns over the long run.

### 2\. Are you able to contribute more than your match?

Maybe maxing out is not right for you but you feel comfortable contributing more than what’s required to earn your match. As we discussed earlier in this article, there is also not a single formula for determining an employer’s match, and therefore it may be possible for you to budget in a higher contribution amount (within the annual limits of course). To that we say “go forth and contribute”.

While you may not get more from your employer once you exceed your matching requirement, contributing more than your match allows you to not only save more, but also take greater advantage of your tax-advantaged account and compounding returns. That small change today may not feel like much, but could create a ripple effect come time for retirement.

We know that life happens and unexpected expenses come up. Know that you can [change your contribution amount at any time](https://help.guideline.com/en/articles/8640267-how-do-i-change-my-401-k-contribution-rate) - that goes for both increasing and decreasing.

When determining how much more you could possibly contribute towards your 401(k), it may be helpful to:

**Examine your expenses:** Add up your average monthly expenses like rent or mortgage, utilities, food and entertainment. Make sure to include any student loans or credit card debt you’re paying down.

**Chart your goals:** It may be helpful to consider retirement alongside a series of other milestones (like buying a home, raising children, going on vacations) and even unplanned expenditures (like medical bills) that have meaningful financial commitments on your path to retirement.

- As we covered in this [article](https://www.guideline.com/education/articles/compound-interest-dollar-cost-averaging), determine your risk tolerance and time to your goals as you consider saving for short and long term goals.

- While a volatile market might be cause for concern, continued and consistent contributions allow you to invest via [dollar-cost averaging](https://www.guideline.com/education/articles/compound-interest-dollar-cost-averaging), helping you to, in theory, reduce the overall impact that market volatility has on the price you pay to acquire more shares of your investments.

**Explore your options:** Just like retirement should be considered alongside other short and long term goals, retirement savings accounts can be considered to be one part of your broader financial portfolio. Exploring other savings and investing options that fit your needs and adjusting as needed as your plans evolve can be effective. Moreover, take some time to learn more about other factors that can impact and help you on your broader financial journey:

- Overall risk tolerance

- Investment objective

- Overall financial situation

- Outside investment and retirement accounts

- Prior investment experience

- Tax bracket

- Time horizon

### 3\. Are you maxing out on your 401(k) contributions?

First things first — if you have a match, maxing out too early in the year can lead to missing out on a portion of your employer’s match. Once you max out and are no longer able to contribute for that tax year, your employer’s match will stop as well. In your Guideline account’s [contribution setting page](https://my.guideline.com/participant/dashboard/portfolio/contribution), we’ll alert you if the amount you’ve elected to contribute will push you into this territory so you can adjust your deferral amount and get the most value from your Guideline 401(k) each year.

Now, if you are already contributing the maximum allowable amount to your 401(k) (\$24,500 in 2026, \$32,500 if you are 50+, and \$35,750 if you’re 60-63) and looking to save more with a dedicated retirement account, consider contributing to an [IRA](https://www.guideline.com/ira).1 IRAs offer similar advantages to a 401(k) and allow you to contribute an additional \$7,500 (\$8,600 if 50+) in 2026. In addition to this uppermost limit, there are contribution limits and considerations based on your income, which are covered [here](https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits?ref=guideline.com).

**Takeaways:**

- **Meet your match**: By not contributing the minimum amount required to meet your match, you are effectively leaving money on the table. While it may not seem consequential today, when you consider the effect of [compound returns](https://www.guideline.com/education/articles/compound-interest-dollar-cost-averaging), a few percentage points today can in theory grow into a meaningful sum by the time you retire.

- **Optimize your max**: If you have an employer match, don’t max out too early in the year, as you may leave some of your match on the table.

- **Don’t exceed the max**: Be mindful of the annual contribution limit, especially if you have access to more than one 401(k) account in a single tax year. Over-contributing requires you to return the excess amount in due time to avoid paying taxes twice and avoid a 10% penalty. Depending on when this takes place, you may need to request a new W2 to ensure your taxable income is correct on your tax return. You can learn more about the process [here.](https://help.guideline.com/en/articles/8605068-what-happens-if-i-overcontribute-to-my-401-k-account)

- **Strike the right balance**: Finances are an incredibly personal topic. Consider your bigger picture — as detailed or as broad as you're comfortable with — and what other financial commitments you may have up ahead. You can change your contribution amount at any time. So, if you’ve decided to contribute 10% but you have an unexpected financial expense and need to scale back for a few months (but not below your match of course), that’s certainly allowable.

Give your employees a roadmap to retirement

With Guideline, you can provide an impactful work benefit while minimizing paperwork and fees.

[Get started](https://my.guideline.com/explore/get-started?gl_cta=%2Feducation%2Farticles%2Fhow-much-should-i-contribute-to-my-401-k&returnUrl=https%3A%2F%2Fwww.guideline.com%2Feducation%2Farticles%2Fhow-much-should-i-contribute-to-my-401-k&source=%2Feducation%2Farticles%2Fhow-much-should-i-contribute-to-my-401-k&token=schedule-demo)

***

[Related articles](https://www.guideline.com/education/audiences/savers)

[See more](https://www.guideline.com/education/audiences/savers)

[ How much can you contribute to a 401(k) in 2024?  Jeff Rosenberger, PhD •5 min](https://www.guideline.com/education/articles/how-much-can-you-contribute-to-a-401-k-in-2024)

[ Is it time to rebalance my 401(k)?  Guideline Team •7 min](https://www.guideline.com/education/articles/is-it-time-to-rebalance-my-401-k)

[ What should you do with your old 401(k)?  Jeff Rosenberger, PhD •6 min](https://www.guideline.com/education/articles/what-should-you-do-with-your-old-401-k-the-3-main-options)

[ How much can you contribute to a 401(k) in 2024?  Jeff Rosenberger, PhD •5 min](https://www.guideline.com/education/articles/how-much-can-you-contribute-to-a-401-k-in-2024)

[ Is it time to rebalance my 401(k)?  Guideline Team •7 min](https://www.guideline.com/education/articles/is-it-time-to-rebalance-my-401-k)

[ What should you do with your old 401(k)?  Jeff Rosenberger, PhD •6 min](https://www.guideline.com/education/articles/what-should-you-do-with-your-old-401-k-the-3-main-options)

[ It might not be too late to contribute to last year’s IRA  Guideline Team •5 min](https://www.guideline.com/education/articles/carryback-contributions)

[See more](https://www.guideline.com/education/audiences/savers)

Search retirement topics

- 1

Subject to IRS cost-of-living adjustments

- The information provided herein is general in nature and is for informational purposes only. It should not be used as a substitute for specific tax advice that considers all relevant facts and circumstances. Guideline makes no representations or guarantees with regard to investment performance as investing involves risk and investments may lose value. Clients should consult a qualified investment or tax professional to determine the appropriate strategy for them.

This website contains content from Guideline, LLC and its subsidiaries, each a separate entity with different regulatory marketing requirements and standards. References to “our” or “we” on this website refer solely to Guideline RK, LLC unless otherwise specifically stated.

The information in this website is for informational purposes only and is not intended to be an offer, recommendation, investment advice, legal or tax advice, or a solicitation to buy or sell any security. By using this website, you agree to Guideline, LLC’s [Privacy Policy](https://my.guideline.com/agreements/privacy) and [Terms and Conditions of Use](https://my.guideline.com/agreements/tos). Neither Guideline, LLC nor its affiliates, are responsible for information provided by third parties. Information included herein from third parties is believed to be reliable however Guideline, LLC does not guarantee the accuracy and completeness of that information.

Guideline, LLC is a holding company, wholly-owned by Gusto, Inc. (“Gusto”), that through its subsidiaries, it provides an integrated platform to companies who seek to work with 1) Guideline RK, LLC (“Guideline”) and/or 2) Guideline Investments, LLC, an SEC Registered Investment Adviser (“Guideline Investments”), both of which are wholly owned by Guideline, LLC.

Neither Gusto nor Guideline, LLC or Guideline RK, LLC is involved in securities activities and is not registered with the SEC or FINRA. Neither Gusto, nor any of its affiliates, is a bank.

Investment advisory services for Gusto’s 401(k) products (when 3(38) fiduciary services are selected) and SEP IRA/IRA products are offered by Guideline Investments, LLC (“Guideline Investments”), an SEC-registered investment adviser. For more information regarding fees and services, see Guideline Investments’, [ADV 2A Brochure](https://www.guideline.com/adv) and [Form CRS](https://www.guideline.com/public-assets/ext/Guideline%20Investments%20Form%20CRS.pdf?v=3). References throughout this website to investment advisory services including but not limited to: investments offered, portfolios, managed portfolios, investment philosophy, assets under management (AUM), annual account fees expressed as a percentage of AUM, suitability questionnaire, 3(38) investment advisory management fiduciary services, robo-advisory services, and investment advice, unless otherwise specifically stated, are services provided by Guideline Investments. Investing involves risk and may lose money, including loss of principal. Investing is not guaranteed and past performance is not a guarantee of future performance. The investment options offered by Guideline Investments are not FDIC insured.

Administrative and recordkeeping services for Gusto’s 401(k) products, and SEP IRA/IRA products, are offered by Guideline RK, LLC (“Guideline”). 3(16) plan administration services are also offered by Guideline and only made available to clients who use the integration services available through Gusto’s payroll services. For more information on Guideline’s pricing, see [here](https://my.guideline.com/agreements/fees). Guideline uses a third-party to provide custodial services. Custodial fees are paid by Guideline.

Any graphs, charts, and other visual aids (collectively referred to as “image(s)”) are provided for information purposes only. None of these images can of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no image can capture all factors and variables required in making such decisions. Investing involves risk, including loss of principal.

© 2026 Guideline, LLC All rights reserved

***

[](https://www.guideline.com/)

- ## Resources

- [Investment funds](https://www.guideline.com/funds)

- [Blog](https://www.guideline.com/education)

- [Help Center](https://help.guideline.com/en)

- ## Company

- [Contact us](https://www.guideline.com/contact-us)

- [Privacy](https://my.guideline.com/agreements/privacy)

- [Terms and Conditions of Use](https://my.guideline.com/agreements/tos)

- [Legal disclosures](https://www.guideline.com/legal)

- [Your privacy choices](https://privacyportal.onetrust.com/webform/29f8c744-2fa0-46a7-b5e8-87783cdf8022/9d3152a7-64d4-4633-a555-3e7f64aea89f)

[](https://www.guideline.com/)

- [](https://www.facebook.com/guideline401k)

- [](https://www.instagram.com/guideline401k_)

- [](https://www.linkedin.com/company/guideline)

- [](https://x.com/guideline401k)

- [](https://apps.apple.com/us/app/guideline/id6446659674)

- [](https://play.google.com/store/apps/details?id=com.guideline.mobile)

- [Privacy](https://my.guideline.com/agreements/privacy)

- [Terms and Conditions of Use](https://my.guideline.com/agreements/tos)

- [Legal disclosures](https://www.guideline.com/legal)

- [Your privacy choices](https://privacyportal.onetrust.com/webform/29f8c744-2fa0-46a7-b5e8-87783cdf8022/9d3152a7-64d4-4633-a555-3e7f64aea89f) | |||||||||

| Readable Markdown | When it comes to the question of how much you should contribute to your 401(k) account, there’s no right or wrong answer. At Guideline, our goal is to provide everyone with a path to retirement, and what that path looks like could change based on your personal goals and circumstances.

And whether you’re just getting started with a 401(k) for the first time or you’re a bit farther along in your journey, it’s never too late or too early to learn more about saving for retirement. As with any financial decision, consulting with an advisor or tax professional can help determine what's best for you.

Let’s talk about your 401(k)**.** Keep reading to learn more about:

- Maximum allowable contributions

- Employer match

- Factors to help you determine what might be the right amount for you

## Know your limits

The IRS — not your employer or your retirement account brokerage — sets the maximum amount an individual may contribute to their 401(k) each year. As we covered in [this article](https://www.guideline.com/education/articles/difference-between-traditional-and-roth-401k), there are tax advantages to contributing to a 401(k) and these contribution limits are put in place by the IRS to ensure those tax advantages are enjoyed fairly by everyone.

### What is the maximum amount I can contribute to my 401(k) each year?

Known as the 402(g) limit in the Internal Revenue Code (or IRC), individuals can contribute up to \$24,500 between their traditional and Roth 401(k) accounts in 2026. If you’re 50 or older, you can contribute an additional \$8,000 (\$32,500 in total) thanks to what’s known as a catch-up contribution.1 And beginning in 2025, there is now an extended catch-up allowing individuals aged 60-63 to contribute \$11,250 (for a total of \$35,750 in 2026).1

While these limits may stay the same some years, they are re-evaluated by the IRS every year to consider cost-of-living adjustments and are subject to change annually.

### Does that limit include what my employer contributes as well?

It’s important to note that these limits only account for what you as an individual saver are contributing to your account, not the amount an employer may be contributing on your behalf. The total amount that can be contributed to your 401(k), also known as the 415(c) limit, inclusive of both your own paycheck deferrals and any employer contributions, is \$72,000 in 2026. That limit increases to \$80,000 if you are 50 or older (and \$83,250 if you’re 60-63 and eligible for the extended catchup). The IRS also stipulates that your 401(k) contributions may not exceed 100% of your taxable income.

The 415(c) limit is reevaluated and typically increases alongside the 402(g) limit annually.

### If I have access to more than one 401(k) in a single year, does that change how much I can contribute?

Since the deferral limits are individual limits, they apply to all of your contributions in a given tax year. Therefore, if you switch jobs halfway through the year, your deferral limit does not reset.

It’s important to tell a new provider of any 401(k) contributions you might have made to date when enrolling to avoid over-contributing by accident. More on this below.

Let’s review these limits with two examples:

- In 2026, a 39-year-old is employed by two companies, both of which offer a 401(k) benefit: Company A from January through September and Company B from October through December. They’ve already contributed \$10,000 to their 401(k) with Company A. Therefore, when enrolling with Company B’s 401(k) provider, it’s important to remember that the limit does not reset and that they cannot exceed the \$24,500 limit. One way to avoid over-contributing is making sure to inform Company B’s 401(k) provider of the \$10,000 already contributed that year.

- Now, a 53-year-old is employed full time by two companies in the same year, both of which offer a 401(k) benefit. In addition to their full-time jobs, they have been hired in a part-time seasonal role for the holidays, and that company offers a 401(k) to their part-time employees. This individual saver is already tracking towards contributing \$24,500 to their 401(k) between Company A and Company B. Therefore, when enrolling with Company C’s 401(k) provider, any additional contributions cannot exceed \$8,000 (based on the IRS’ contribution limits with catch-up contributions for 2026).

### Do rolled over funds count towards my contribution limit?

It depends. If you made the contribution in the same tax year, then the amount you contributed will count towards your contribution limit, regardless if you rolled them over. If you have rolled over funds from a previous 401(k), but made the contribution in a previous tax year, that balance does not count towards your annual limit.

For example, let’s say you were employed at Company X over the course of two calendar years from April 2024 to April 2025, and then you joined Company Y in May 2025. Any contributions you made from April 2024 until December 31, 2024 would not count towards your 2025 limit, even if you roll it over to your Company Y 401(k) in 2025 (or any year thereafter).1

### What happens if I contribute above the IRS-allowable amount?

You could end up being taxed twice. Given the tax savings 401(k)s offer, the [IRS has consequences](https://www.irs.gov/retirement-plans/consequences-to-a-participant-who-makes-excess-deferrals-to-a-401k-plan?ref=guideline.com), in the form of taxes, when plan participants exceed the allowable limit. While this may happen for a few reasons, a common reason is for not informing a second 401(k) provider of any contributions already made (or planned to make) in that tax year.

Guideline monitors your activity throughout the year and will notify you if you do exceed your limit for deferrals we are aware of. You can learn more about the process [here](https://help.guideline.com/en/articles/8605068-what-happens-if-i-overcontribute-to-my-401-k-account).

## Meeting your match

You may have heard this before, and no, we’re not talking about your other half.

### What is a match and how can I meet it?

Depending on your employer’s 401(k) benefit, you may have access to what’s known as an ‘employer match’. It’s more or less what it sounds like - the employer will match your own contributions (also known as deferrals, since you’re deferring an amount from your salary) up to a certain amount.

This can take a few different forms, so it’s important to pay attention to what is required in order to earn the full amount of the match in your plan. Common examples of an employer match are:

**Single-tier formula:** The employer matches the same amount for each dollar that you contribute, up to a certain percentage of your income.

Example A: Your employer matches 50% of the first 6% of your contributions. In this case, you need to contribute at least 6% per-pay-period to earn your full match. Here, the employer is matching \$.50 for each \$1, up to 6% of your income.

Example B: Your employer matches 100% of the first 3% of your contributions. Therefore, you need to contribute at least 3% per-pay-period to earn your full match. Here, the employer is matching \$1 for each \$1 up to 3% of your income.

In both cases, the employer’s match is 3% of the employee’s income, but in the first example you would need to defer at least 6% to get the full 3% match.

**Multi-tier formula:** The employer’s match may have different tiers, where the first tier is matched at one [ratio and subsequent tiers may be matched at different ratios](https://www.guideline.com/education/articles/understanding-401-k-expense-ratios-and-why-they-matter).

Example C: Your employer matches 100% on the first 2% and 50% on the next 2%. Therefore, you need to contribute at least 4% in order to earn the full match of 3%. Here, the employer is matching \$1 for \$1 on the first 2% contributed, and \$.50 for each \$1 contributed on the next 2%. In this example too, the employer’s match is 3% of the employee's income but you would need to defer at least 4% to get the full 3% match.

In both the single-tier and multi-tier formulas, any contributions made beyond what is required to earn the employer’s match, will not result in a higher match.

### Why is it important to meet the match?

It can be helpful to think of your employer’s contribution to your 401(k) as part of your total salary. Therefore, if offered a match, it may be important to consider doing what you can to contribute the minimum amount required to earn your employer’s full match. By not meeting your match, you are effectively leaving money on the table and not earning your full wages. If we take a look back at the examples above - if one’s income is \$50,000, by not contributing enough to meet their match, they could be leaving up to \$1,500 of employer contributions to their retirement behind.

### Can I contribute more than my match?

You can absolutely contribute more than your match, and it’s a great way to save more towards retirement while taking advantage of those tax-advantages. Do note that anything you contribute beyond what your employer matches will not earn any additional match.

### Is the matched amount mine to take with me if I leave my employer?

It depends on your employer’s plan. Some employers may opt to include a vesting requirement, which may delay when you will have full access to your employer’s match. Just like the match formula can vary from plan to plan, so can the vesting schedule.

There are three types of vesting schedules:

- **Immediate vesting**: In this case, there is no term of employment required to earn your employer’s match.

- [**Cliff vesting**](https://help.guideline.com/en/articles/8593684-what-is-a-cliff-vesting-schedule)**:** After a predetermined amount of time, you unlock the full amount of your employer's match. For example, iIf you have a 2-year cliff, you unlock the full amount of your employer’s match after your 2 year anniversary with the company.

- [**Graded vesting**](https://help.guideline.com/en/articles/8593694-what-is-a-graded-vesting-schedule)**:** There’s a bit more flexibility on the employer’s part here and can differ by plan. Generally, you gradually unlock a portion each year you are employed by your employer. It’s always good to familiarize yourself with your plan’s vesting schedule. Using the same 2-years as an example, if you have a 2-year graded vesting with equal vesting each year, you unlock the 50% of your employer’s match after your 1st year with the company, and 100% of your match after 2 years with the company.

Know that if your 401(k) plan has a vesting requirement and your match has not fully vested before you part ways with your employer, it only impacts the employer’s match, not what you contributed. Whatever you as the employee contributed to your account - including gains and losses - is yours to take with you as you continue on, regardless of vesting.

## Finding your ‘just right’

Personal finances are just that - personal. There is not a single ‘right’ amount that everybody should be contributing to their retirement savings. There are, however, questions to help you in determining what might be the right amount for you.

### 1\. Are you meeting your match?

We’ve said it before, and we’ll say it again. When evaluating your finances, it can be important to consider contributing the minimum amount required by your employer's plan to earn the full match. Not doing so is equivalent to not earning your full salary. While this may reduce your take-home pay, consider the growth potential of your retirement account from compound returns over the long run.

### 2\. Are you able to contribute more than your match?

Maybe maxing out is not right for you but you feel comfortable contributing more than what’s required to earn your match. As we discussed earlier in this article, there is also not a single formula for determining an employer’s match, and therefore it may be possible for you to budget in a higher contribution amount (within the annual limits of course). To that we say “go forth and contribute”.

While you may not get more from your employer once you exceed your matching requirement, contributing more than your match allows you to not only save more, but also take greater advantage of your tax-advantaged account and compounding returns. That small change today may not feel like much, but could create a ripple effect come time for retirement.

We know that life happens and unexpected expenses come up. Know that you can [change your contribution amount at any time](https://help.guideline.com/en/articles/8640267-how-do-i-change-my-401-k-contribution-rate) - that goes for both increasing and decreasing.

When determining how much more you could possibly contribute towards your 401(k), it may be helpful to:

**Examine your expenses:** Add up your average monthly expenses like rent or mortgage, utilities, food and entertainment. Make sure to include any student loans or credit card debt you’re paying down.

**Chart your goals:** It may be helpful to consider retirement alongside a series of other milestones (like buying a home, raising children, going on vacations) and even unplanned expenditures (like medical bills) that have meaningful financial commitments on your path to retirement.

- As we covered in this [article](https://www.guideline.com/education/articles/compound-interest-dollar-cost-averaging), determine your risk tolerance and time to your goals as you consider saving for short and long term goals.

- While a volatile market might be cause for concern, continued and consistent contributions allow you to invest via [dollar-cost averaging](https://www.guideline.com/education/articles/compound-interest-dollar-cost-averaging), helping you to, in theory, reduce the overall impact that market volatility has on the price you pay to acquire more shares of your investments.

**Explore your options:** Just like retirement should be considered alongside other short and long term goals, retirement savings accounts can be considered to be one part of your broader financial portfolio. Exploring other savings and investing options that fit your needs and adjusting as needed as your plans evolve can be effective. Moreover, take some time to learn more about other factors that can impact and help you on your broader financial journey:

- Overall risk tolerance

- Investment objective

- Overall financial situation

- Outside investment and retirement accounts

- Prior investment experience

- Tax bracket

- Time horizon

### 3\. Are you maxing out on your 401(k) contributions?

First things first — if you have a match, maxing out too early in the year can lead to missing out on a portion of your employer’s match. Once you max out and are no longer able to contribute for that tax year, your employer’s match will stop as well. In your Guideline account’s [contribution setting page](https://my.guideline.com/participant/dashboard/portfolio/contribution), we’ll alert you if the amount you’ve elected to contribute will push you into this territory so you can adjust your deferral amount and get the most value from your Guideline 401(k) each year.

Now, if you are already contributing the maximum allowable amount to your 401(k) (\$24,500 in 2026, \$32,500 if you are 50+, and \$35,750 if you’re 60-63) and looking to save more with a dedicated retirement account, consider contributing to an [IRA](https://www.guideline.com/ira).1 IRAs offer similar advantages to a 401(k) and allow you to contribute an additional \$7,500 (\$8,600 if 50+) in 2026. In addition to this uppermost limit, there are contribution limits and considerations based on your income, which are covered [here](https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits?ref=guideline.com).

**Takeaways:**

- **Meet your match**: By not contributing the minimum amount required to meet your match, you are effectively leaving money on the table. While it may not seem consequential today, when you consider the effect of [compound returns](https://www.guideline.com/education/articles/compound-interest-dollar-cost-averaging), a few percentage points today can in theory grow into a meaningful sum by the time you retire.

- **Optimize your max**: If you have an employer match, don’t max out too early in the year, as you may leave some of your match on the table.

- **Don’t exceed the max**: Be mindful of the annual contribution limit, especially if you have access to more than one 401(k) account in a single tax year. Over-contributing requires you to return the excess amount in due time to avoid paying taxes twice and avoid a 10% penalty. Depending on when this takes place, you may need to request a new W2 to ensure your taxable income is correct on your tax return. You can learn more about the process [here.](https://help.guideline.com/en/articles/8605068-what-happens-if-i-overcontribute-to-my-401-k-account)

- **Strike the right balance**: Finances are an incredibly personal topic. Consider your bigger picture — as detailed or as broad as you're comfortable with — and what other financial commitments you may have up ahead. You can change your contribution amount at any time. So, if you’ve decided to contribute 10% but you have an unexpected financial expense and need to scale back for a few months (but not below your match of course), that’s certainly allowable.

Give your employees a roadmap to retirement

With Guideline, you can provide an impactful work benefit while minimizing paperwork and fees. | |||||||||

| ML Classification | ||||||||||

| ML Categories |

Raw JSON{

"/Finance": 993,

"/Finance/Financial_Planning_and_Management": 825,

"/Finance/Financial_Planning_and_Management/Retirement_and_Pension": 823

} | |||||||||

| ML Page Types |

Raw JSON{

"/Article": 993,

"/Article/How_to": 507

} | |||||||||

| ML Intent Types |

Raw JSON{

"Informational": 996,

"Commercial": 107

} | |||||||||

| Content Metadata | ||||||||||

| Language | en-us | |||||||||

| Author | null | |||||||||

| Publish Time | 2025-03-13 00:00:00 (1 year ago) | |||||||||

| Original Publish Time | 2024-08-09 16:49:48 (1 year ago) | |||||||||

| Republished | Yes | |||||||||

| Word Count (Total) | 3,518 | |||||||||

| Word Count (Content) | 2,761 | |||||||||

| Links | ||||||||||

| External Links | 12 | |||||||||

| Internal Links | 42 | |||||||||

| Technical SEO | ||||||||||

| Meta Nofollow | No | |||||||||

| Meta Noarchive | No | |||||||||

| JS Rendered | Yes | |||||||||

| Redirect Target | null | |||||||||

| Performance | ||||||||||

| Download Time (ms) | 145 | |||||||||

| TTFB (ms) | 133 | |||||||||

| Download Size (bytes) | 42,153 | |||||||||

| Shard | 44 (laksa) | |||||||||

| Root Hash | 5639064991638572844 | |||||||||

| Unparsed URL | com,guideline!www,/education/articles/how-much-should-i-contribute-to-my-401-k s443 | |||||||||