ℹ️ Skipped - page is already crawled

| Filter | Status | Condition | Details |

|---|---|---|---|

| HTTP status | PASS | download_http_code = 200 | HTTP 200 |

| Age cutoff | PASS | download_stamp > now() - 6 MONTH | 0 months ago |

| History drop | PASS | isNull(history_drop_reason) | No drop reason |

| Spam/ban | PASS | fh_dont_index != 1 AND ml_spam_score = 0 | ml_spam_score=0 |

| Canonical | PASS | meta_canonical IS NULL OR = '' OR = src_unparsed | Not set |

| Property | Value |

|---|---|

| URL | https://www.fidelity.com/viewpoints/retirement/401k-contributions |

| Last Crawled | 2026-04-10 21:30:17 (14 hours ago) |

| First Indexed | 2019-09-23 18:54:55 (6 years ago) |

| HTTP Status Code | 200 |

| Meta Title | After-tax 401(k) contributions | Retirement benefits | Fidelity |

| Meta Description | Making after-tax contributions allows you to invest more money with the potential for tax-deferred growth. That's a great benefit on its own - learn more here. |

| Meta Canonical | null |

| Boilerpipe Text | What to do with after-tax 401(k) contributions

This strategy could make it worthwhile to keep saving above the annual limit.

Key takeaways

After contributing up to the annual limit in your 401(k), you may be able to save even more on an after-tax basis if your plan allows.

Earnings on after-tax contributions are considered pre-tax and would grow tax-deferred until withdrawals begin.

Converting after-tax 401(k) contributions to a Roth account is an option. After converting to a Roth, earnings can grow and be distributed tax-free if certain requirements are met.

You already know about the benefits of saving in your workplace savings plan, like a 401(k). But you may be able to save more than you think—for many people, the annual contribution limit isn't the end of their tax-advantaged saving opportunities.

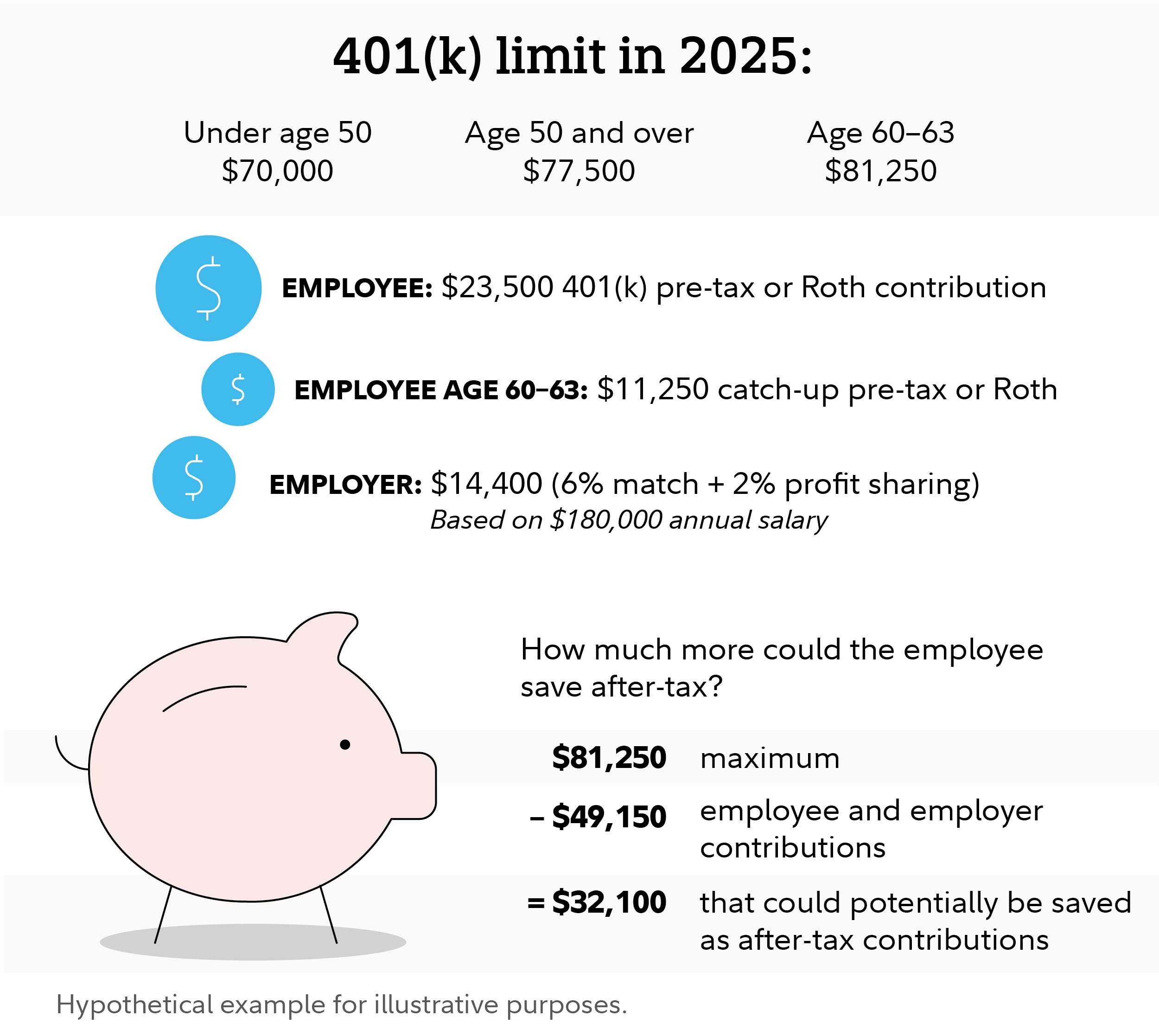

In 2025, you can contribute up to $23,500 to your 401(k). Your contributions can be entirely pre-tax or Roth (if your plan allows for Roth contributions), or some combination of the two. If you're at least age 50 by the end of the calendar year, you can add a catch-up contribution of $7,500 pre-tax. And if you're between ages 60 and 63, you will be eligible to contribute up to $11,250 as a catch-up contribution, if your plan allows.

Unlike Roth IRAs, there are no income caps on Roth contributions in a workplace savings account like a 401(k). Once you see that you will max out your contributions, you may want to consider making after-tax contributions if your plan allows. These are a third type of contribution to your workplace savings plan, in addition to pre-tax and Roth.

One quick note about after-tax contributions—you may not have to wait until you’ve hit the annual contribution limit during the year to make them. After-tax contributions can be made at the same time as your regular contributions—just be sure that your after-tax contributions aren't set so high that they will prevent you from fully making pre-tax and Roth contributions first. Check with your plan administrator if the rules seem unclear.

Be aware also that there is an annual maximum limit on contributions from all sources—including your employer. As you’re calculating the amount you can contribute, include any matching or profit sharing/non-elective contributions from your employer so that “free money” contribution doesn’t get crowded out.

The IRS allows a total of up to $70,000 of employer and employee contributions to be saved in a 401(k) for 2025, plus any age-dependent employee catch-up contributions. Here's what's included:

What you save

Elective deferrals (either tax-deferred, Roth, or a combination)

Optional after-tax contributions to your workplace savings plan beyond the annual elective deferral limit (if allowed by your employer)

What your employer can contribute on your behalf

Employer matching contributions

Employer nonelective contributions, typically profit sharing

Sign up for

Fidelity Viewpoints

weekly email for our latest insights.

After-tax contributions to your workplace plan can be withdrawn without taxes or penalties. Any earnings on those after-tax contributions are considered pre-tax balances—so taxes would have to be paid on withdrawals of the earnings and there may be a 10% penalty if you're under age 59½.

What you should know is that you won't be able to withdraw your after-tax contributions without also withdrawing any earnings associated with them. Taking out just the after-tax balance would not be allowed (unless they are rolled over to an IRA).

Let's say you made $10,000 in after-tax contributions and that money earned $2,000 in returns. In order to withdraw the $10,000, the $2,000 in earnings would need to be withdrawn as well. And that applies if you are converting the after-tax balance as well (if you are converting in-plan).

With respect to federal taxation only. Distributions may or may not be subject to state taxation.

Potential strategies for after-tax 401(k) contributions

Making after-tax contributions allows you to invest more money with the potential for tax-deferred growth. That's a powerful benefit on its own—but that's not the end of the story. You could then go a step further and convert your after-tax contributions to a Roth account. There are a couple of different ways to accomplish that (if your employer permits), including rolling over your balances to an IRA or doing an in-plan conversion if it's offered by your employer along with a Roth option.

When you convert after-tax balances to Roth, no taxes would be due on the conversion of your contributions. However, when you convert, you have to include associated earnings, which would be subject to tax. So, if the option is available to you, you may want to roll those earnings to a traditional IRA instead. That strategy is covered more in subsequent sections.

Earnings in a Roth account grow and may potentially be distributed tax-free as long as certain conditions are met. So no taxes would be due on withdrawals—as long as they take place after age 59½ and the

5-year aging requirement

has been met.

Satisfying the 5-year aging requirement for the tax-free withdrawal of earnings means that there are at least 5 years between either the year of your first Roth contribution or the year the conversion took place and any withdrawals. The 5-year clock starts on January 1 of the tax year in which the conversion occurred or the contribution was made, no matter when during the year it actually happened. So if you converted in December, the aging requirement might, in practice, be only a bit more than 4 years.

Not all employers offer a Roth option in their retirement plan—or they may not offer the option to do an in-plan conversion. If your employer does not offer a Roth option or the in-plan Roth conversion feature, you can still roll over your after-tax contributions to a Roth IRA. Here are the 3 strategies. The options available to you will depend on your situation.

1. In-plan Roth conversion

Many employers do offer a Roth option in their retirement plan. And some plans allow you to do an in-plan conversion.

An in-plan Roth conversion allows you to take after-tax contributions and convert them to Roth. Some employers even offer an auto-convert feature inside their plan. You can set it up so that any after-tax contributions are automatically converted to a Roth at regular intervals. Though after-tax contributions have already been taxed, any earnings associated with them have not—so converting earnings will trigger a tax bill in the year of the conversion.

2. Rolling out to IRAs after an in-plan conversion

After completing a Roth conversion within your workplace retirement plan, rolling out to IRAs should be relatively straightforward if you choose to do that. If you’re planning to roll the money out to a Roth IRA at some point and don’t already contribute to a Roth IRA, it may make sense to open an account and make at least one contribution now, if possible, so the 5-year clock starts ticking on this account. Roth 401(k)s have a 5-year aging requirement as well that is tracked separately from Roth IRAs. These rules don't need to be subsequently met again in the future, unlike Roth conversions, which have a new 5-year clock for each converted amount (however, the earnings follow the rule for either the plan or the Roth IRA).

If you earn too much to contribute to a Roth IRA, you do have options. Read

Viewpoints

on Fidelity.com:

Do you earn too much for a Roth IRA?

3. IRA rollover without an in-plan conversion

You can roll over after-tax contributions to a Roth IRA, and it is possible to do that before age 59½. There is a big catch, though: Not all plans allow withdrawals while you’re still with the company, and your retirement plan may have some rules around the requirements for rolling out of the plan. In-service withdrawals come with some potentially complicated rules, so it’s important to understand the rules the IRS has and those of your retirement plan.

In general, to roll after-tax money to a Roth IRA, earnings on the after-tax balance must, in most cases, also be withdrawn. You may have a few options.

If you have both pre-tax and after-tax contributions, you may be able to take a partial distribution from your retirement plan, consisting of just one or the other, if the plan separately tracks the sources of all of your contributions. In that case, you may want to roll out only the after-tax source balances directly into a Roth IRA.

The pre-tax contributions, along with the earnings from both the pre-tax and the after-tax contributions, can be rolled to a traditional IRA, incurring no current income tax.

Alternatively, you can roll everything into a Roth IRA, but you would need to pay income taxes on the pre-tax contributions and all of the earnings.

Important note: Any partial withdrawals or in-plan conversions may affect eligibility for

net unrealized appreciation

treatment on appreciated employer stock held in the plan.

It's advisable to consult with a financial advisor before making any decisions.

To find out more, read

Viewpoints

on Fidelity.com:

Rolling after-tax money in a 401(k) to a Roth IRA

Be sure to consider all your options

Making after-tax contributions and then converting to Roth may seem complicated, but the long-term benefits can make it worthwhile. But bear in mind: there can be benefits to keeping your money in the workplace savings plan. Balances in your workplace retirement account may be available for loans, if your plan allows them, while balances in an IRA are not. On the other hand, IRAs have certain advantages as well. For instance, you may be able to get a broader range of investment choices. So it's a good idea to check with your financial advisor and tax advisor before choosing a strategy. |

| Markdown | [Skip to main content](https://www.fidelity.com/viewpoints/retirement/401k-contributions#navSkipToContent)

[Fidelity.com Home](https://www.fidelity.com/)

[Log in](https://digital.fidelity.com/prgw/digital/login/full-page)

- [Accounts & Trade]()

- [Portfolio](https://digital.fidelity.com/prgw/digital/login/full-page?AuthRedUrl=https://digital.fidelity.com/ftgw/digital/portfolio/summary)

- [Account Positions](https://digital.fidelity.com/ftgw/digital/portfolio/positions)

- [Trade](https://digital.fidelity.com/ftgw/digital/trade-equity/index/orderEntry)

- [Fidelity Trader+ Web](https://digital.fidelity.com/ftgw/digital/trader-dashboard)

- [Fidelity Trader+](https://www.fidelity.com/trading/trading-platforms)

- [Transfers](https://www.fidelity.com/customer-service/money-movement)

- [Cash Management](https://digital.fidelity.com/ftgw/digital/cashmanagement)

- [Bill Pay](https://digital.fidelity.com/ftgw/digital/billpay/home)

- [Full View®](https://digital.fidelity.com/ftgw/pna/customer/pgc/networth/)

- [Security Settings](https://digital.fidelity.com/ftgw/digital/security/dashboard/view)

- [Account Features](https://digital.fidelity.com/ftgw/digital/portfolio/features)

- [Documents](https://digital.fidelity.com/ftgw/digital/portfolio/documents)

- [Tax Forms & Information](https://www.fidelity.com/tax-information/overview)

- [Retirement Distributions](https://digital.fidelity.com/ftgw/digital/mrdhub)

- [Refer a Friend](https://www.fidelity.com/customer-service/friendsandfamily3a)

- [Retirement]()

- [Retirement Planning](https://www.fidelity.com/retirement/retirement-planning)

- [401(k) Rollovers & IRA Transfers](https://www.fidelity.com/retirement/401k-rollover)

- [Retirement Accounts](https://www.fidelity.com/retirement/retirement-accounts)

- [Retirement Education](https://www.fidelity.com/learning-center/personal-finance/retirement-education)

- [Wealth Management]()

- [Wealth Management Offerings](https://www.fidelity.com/wealth/wealth-management-offerings)

- [Financial Advisors](https://www.fidelity.com/wealth/financial-advisors)

- [Financial Planning](https://www.fidelity.com/wealth/financial-planning)

- [Investment Management](https://www.fidelity.com/wealth/investment-management)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [News & Research]()

- [News](https://www.fidelity.com/news/overview)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [Watchlist](https://digital.fidelity.com/ftgw/digital/watwebex)

- [Alerts](https://alertable.fidelity.com/ftgw/digital/alerts)

- [Stocks, ETFs, Crypto](https://digital.fidelity.com/prgw/digital/research/src)

- [Mutual Funds](https://fundresearch.fidelity.com/fund-screener)

- [Fixed Income, Bonds & CDs](https://fixedincome.fidelity.com/ftgw/fi/FILanding)

- [Options](https://digital.fidelity.com/ftgw/digital/options-home/)

- [IPOs](https://brokerage.fidelity.com/ftgw/brkg/ipo/calendar)

- [Annuities](https://fundresearch.fidelity.com/fund-screener/annuities/)

- [Learn](https://www.fidelity.com/learning-center/overview)

- [Products]()

- [Spending & Saving](https://www.fidelity.com/spend-save/overview)

- [Investing & Trading](https://www.fidelity.com/trading/overview)

- [Mutual Funds](https://www.fidelity.com/mutual-funds/overview)

- [Crypto](https://www.fidelity.com/crypto/overview)

- [Direct Indexing](https://www.fidelity.com/direct-indexing/overview)

- [Fixed Income, Bonds & CDs](https://www.fidelity.com/fixed-income-bonds/overview)

- [ETFs](https://www.fidelity.com/etfs/investing-in-etfs)

- [Options](https://www.fidelity.com/options-trading/overview)

- [Sustainable Investing](https://www.fidelity.com/sustainable/overview)

- [529 College Savings](https://www.fidelity.com/529-plans/overview)

- [Health Savings Accounts](https://www.fidelity.com/go/hsa/why-hsa)

- [Annuities](https://www.fidelity.com/annuities/overview)

- [Life Insurance](https://www.fidelity.com/life-insurance/term-life-insurance/overview)

- [Customer Service](https://www.fidelity.com/customer-service/overview)

- [Fidelity Assistant](https://www.fidelity.com/customer-service/overview?ccsource=FA_NAV)

- [Profile](https://digital.fidelity.com/ftgw/digital/profile)

[Log in](https://digital.fidelity.com/prgw/digital/login/full-page) [Open an account](https://www.fidelity.com/open-account/overview)

[Fidelity.com Home](https://www.fidelity.com/)

- [Customer Service](https://www.fidelity.com/customer-service/overview)

- [Fidelity Assistant](https://www.fidelity.com/customer-service/overview?ccsource=FA_NAV)

- [Profile](https://digital.fidelity.com/ftgw/digital/profile)

- [Open an account](https://www.fidelity.com/open-account/overview)

- [Log in](https://digital.fidelity.com/prgw/digital/login/full-page)

- [Accounts & Trade]()

- [Portfolio](https://digital.fidelity.com/prgw/digital/login/full-page?AuthRedUrl=https://digital.fidelity.com/ftgw/digital/portfolio/summary)

- [Account Positions](https://digital.fidelity.com/ftgw/digital/portfolio/positions)

- [Trade](https://digital.fidelity.com/ftgw/digital/trade-equity/index/orderEntry)

- [Fidelity Trader+ Web](https://digital.fidelity.com/ftgw/digital/trader-dashboard)

- [Fidelity Trader+](https://www.fidelity.com/trading/trading-platforms)

- [Transfers](https://www.fidelity.com/customer-service/money-movement)

- [Cash Management](https://digital.fidelity.com/ftgw/digital/cashmanagement)

- [Bill Pay](https://digital.fidelity.com/ftgw/digital/billpay/home)

- [Full View®](https://digital.fidelity.com/ftgw/pna/customer/pgc/networth/)

- [Security Settings](https://digital.fidelity.com/ftgw/digital/security/dashboard/view)

- [Account Features](https://digital.fidelity.com/ftgw/digital/portfolio/features)

- [Documents](https://digital.fidelity.com/ftgw/digital/portfolio/documents)

- [Tax Forms & Information](https://www.fidelity.com/tax-information/overview)

- [Retirement Distributions](https://digital.fidelity.com/ftgw/digital/mrdhub)

- [Refer a Friend](https://www.fidelity.com/customer-service/friendsandfamily3a)

- [Retirement]()

- [Retirement Planning](https://www.fidelity.com/retirement/retirement-planning)

- [401(k) Rollovers & IRA Transfers](https://www.fidelity.com/retirement/401k-rollover)

- [Retirement Accounts](https://www.fidelity.com/retirement/retirement-accounts)

- [Retirement Education](https://www.fidelity.com/learning-center/personal-finance/retirement-education)

- [Wealth Management]()

- [Wealth Management Offerings](https://www.fidelity.com/wealth/wealth-management-offerings)

- [Financial Advisors](https://www.fidelity.com/wealth/financial-advisors)

- [Financial Planning](https://www.fidelity.com/wealth/financial-planning)

- [Investment Management](https://www.fidelity.com/wealth/investment-management)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [News & Research]()

- [News](https://www.fidelity.com/news/overview)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [Watchlist](https://digital.fidelity.com/ftgw/digital/watwebex)

- [Alerts](https://alertable.fidelity.com/ftgw/digital/alerts)

- [Stocks, ETFs, Crypto](https://digital.fidelity.com/prgw/digital/research/src)

- [Mutual Funds](https://fundresearch.fidelity.com/fund-screener)

- [Fixed Income, Bonds & CDs](https://fixedincome.fidelity.com/ftgw/fi/FILanding)

- [Options](https://digital.fidelity.com/ftgw/digital/options-home/)

- [IPOs](https://brokerage.fidelity.com/ftgw/brkg/ipo/calendar)

- [Annuities](https://fundresearch.fidelity.com/fund-screener/annuities/)

- [Learn](https://www.fidelity.com/learning-center/overview)

- [Products]()

- [Spending & Saving](https://www.fidelity.com/spend-save/overview)

- [Investing & Trading](https://www.fidelity.com/trading/overview)

- [Mutual Funds](https://www.fidelity.com/mutual-funds/overview)

- [Crypto](https://www.fidelity.com/crypto/overview)

- [Direct Indexing](https://www.fidelity.com/direct-indexing/overview)

- [Fixed Income, Bonds & CDs](https://www.fidelity.com/fixed-income-bonds/overview)

- [ETFs](https://www.fidelity.com/etfs/investing-in-etfs)

- [Options](https://www.fidelity.com/options-trading/overview)

- [Sustainable Investing](https://www.fidelity.com/sustainable/overview)

- [529 College Savings](https://www.fidelity.com/529-plans/overview)

- [Health Savings Accounts](https://www.fidelity.com/go/hsa/why-hsa)

- [Annuities](https://www.fidelity.com/annuities/overview)

- [Life Insurance](https://www.fidelity.com/life-insurance/term-life-insurance/overview)

[Skip to main content](https://www.fidelity.com/viewpoints/retirement/401k-contributions#navSkipToContent)

[Fidelity.com Home](https://www.fidelity.com/)

[Log in](https://digital.fidelity.com/prgw/digital/login/full-page)

- [Accounts & Trade]()

- [Portfolio](https://digital.fidelity.com/prgw/digital/login/full-page?AuthRedUrl=https://digital.fidelity.com/ftgw/digital/portfolio/summary)

- [Account Positions](https://digital.fidelity.com/ftgw/digital/portfolio/positions)

- [Trade](https://digital.fidelity.com/ftgw/digital/trade-equity/index/orderEntry)

- [Fidelity Trader+ Web](https://digital.fidelity.com/ftgw/digital/trader-dashboard)

- [Fidelity Trader+](https://www.fidelity.com/trading/trading-platforms)

- [Transfers](https://www.fidelity.com/customer-service/money-movement)

- [Cash Management](https://digital.fidelity.com/ftgw/digital/cashmanagement)

- [Bill Pay](https://digital.fidelity.com/ftgw/digital/billpay/home)

- [Full View®](https://digital.fidelity.com/ftgw/pna/customer/pgc/networth/)

- [Security Settings](https://digital.fidelity.com/ftgw/digital/security/dashboard/view)

- [Account Features](https://digital.fidelity.com/ftgw/digital/portfolio/features)

- [Documents](https://digital.fidelity.com/ftgw/digital/portfolio/documents)

- [Tax Forms & Information](https://www.fidelity.com/tax-information/overview)

- [Retirement Distributions](https://digital.fidelity.com/ftgw/digital/mrdhub)

- [Refer a Friend](https://www.fidelity.com/customer-service/friendsandfamily3a)

- [Investing]()

- [Self Directed Investing](https://www.fidelity.com/investing/trading)

- [Advanced Trading](https://www.fidelity.com/investing/advanced-trading)

- [Investing for a Child](https://www.fidelity.com/investing/investing-for-kids)

- [Managing Cash & Credit](https://www.fidelity.com/investing/manage-cash-credit-lending)

- [Investment Accounts & Products](https://www.fidelity.com/investing/investment-accounts)

- [Investing & Trading Education](https://www.fidelity.com/learning-center/personal-finance/investing-trading-education)

- [Retirement]()

- [Retirement Planning](https://www.fidelity.com/retirement/retirement-planning)

- [401(k) Rollovers & IRA Transfers](https://www.fidelity.com/retirement/401k-rollover)

- [Retirement Accounts](https://www.fidelity.com/retirement/retirement-accounts)

- [Retirement Education](https://www.fidelity.com/learning-center/personal-finance/retirement-education)

- [Wealth Management]()

- [Wealth Management Offerings](https://www.fidelity.com/wealth/wealth-management-offerings)

- [Financial Advisors](https://www.fidelity.com/wealth/financial-advisors)

- [Financial Planning](https://www.fidelity.com/wealth/financial-planning)

- [Investment Management](https://www.fidelity.com/wealth/investment-management)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [News & Research]()

- [News](https://www.fidelity.com/news/overview)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [Watchlist](https://digital.fidelity.com/ftgw/digital/watwebex)

- [Alerts](https://alertable.fidelity.com/ftgw/digital/alerts)

- [Stocks, ETFs, Crypto](https://digital.fidelity.com/prgw/digital/research/src)

- [Mutual Funds](https://fundresearch.fidelity.com/fund-screener)

- [Fixed Income, Bonds & CDs](https://fixedincome.fidelity.com/ftgw/fi/FILanding)

- [Options](https://digital.fidelity.com/ftgw/digital/options-home/)

- [IPOs](https://brokerage.fidelity.com/ftgw/brkg/ipo/calendar)

- [Annuities](https://fundresearch.fidelity.com/fund-screener/annuities/)

- [Learn](https://www.fidelity.com/learning-center/overview)

- [Customer Service](https://www.fidelity.com/customer-service/overview)

- [Fidelity Assistant](https://www.fidelity.com/customer-service/overview?ccsource=FA_NAV)

- [Profile](https://digital.fidelity.com/ftgw/digital/profile)

[Log in](https://digital.fidelity.com/prgw/digital/login/full-page) [Open an account](https://www.fidelity.com/open-account/overview)

[Fidelity.com Home](https://www.fidelity.com/)

- [Customer Service](https://www.fidelity.com/customer-service/overview)

- [Fidelity Assistant](https://www.fidelity.com/customer-service/overview?ccsource=FA_NAV)

- [Profile](https://digital.fidelity.com/ftgw/digital/profile)

- [Open an account](https://www.fidelity.com/open-account/overview)

- [Log in](https://digital.fidelity.com/prgw/digital/login/full-page)

- [Accounts & Trade]()

- [Portfolio](https://digital.fidelity.com/prgw/digital/login/full-page?AuthRedUrl=https://digital.fidelity.com/ftgw/digital/portfolio/summary)

- [Account Positions](https://digital.fidelity.com/ftgw/digital/portfolio/positions)

- [Trade](https://digital.fidelity.com/ftgw/digital/trade-equity/index/orderEntry)

- [Fidelity Trader+ Web](https://digital.fidelity.com/ftgw/digital/trader-dashboard)

- [Fidelity Trader+](https://www.fidelity.com/trading/trading-platforms)

- [Transfers](https://www.fidelity.com/customer-service/money-movement)

- [Cash Management](https://digital.fidelity.com/ftgw/digital/cashmanagement)

- [Bill Pay](https://digital.fidelity.com/ftgw/digital/billpay/home)

- [Full View®](https://digital.fidelity.com/ftgw/pna/customer/pgc/networth/)

- [Security Settings](https://digital.fidelity.com/ftgw/digital/security/dashboard/view)

- [Account Features](https://digital.fidelity.com/ftgw/digital/portfolio/features)

- [Documents](https://digital.fidelity.com/ftgw/digital/portfolio/documents)

- [Tax Forms & Information](https://www.fidelity.com/tax-information/overview)

- [Retirement Distributions](https://digital.fidelity.com/ftgw/digital/mrdhub)

- [Refer a Friend](https://www.fidelity.com/customer-service/friendsandfamily3a)

- [Investing]()

- [Self Directed Investing](https://www.fidelity.com/investing/trading)

- [Advanced Trading](https://www.fidelity.com/investing/advanced-trading)

- [Investing for a Child](https://www.fidelity.com/investing/investing-for-kids)

- [Managing Cash & Credit](https://www.fidelity.com/investing/manage-cash-credit-lending)

- [Investment Accounts & Products](https://www.fidelity.com/investing/investment-accounts)

- [Investing & Trading Education](https://www.fidelity.com/learning-center/personal-finance/investing-trading-education)

- [Retirement]()

- [Retirement Planning](https://www.fidelity.com/retirement/retirement-planning)

- [401(k) Rollovers & IRA Transfers](https://www.fidelity.com/retirement/401k-rollover)

- [Retirement Accounts](https://www.fidelity.com/retirement/retirement-accounts)

- [Retirement Education](https://www.fidelity.com/learning-center/personal-finance/retirement-education)

- [Wealth Management]()

- [Wealth Management Offerings](https://www.fidelity.com/wealth/wealth-management-offerings)

- [Financial Advisors](https://www.fidelity.com/wealth/financial-advisors)

- [Financial Planning](https://www.fidelity.com/wealth/financial-planning)

- [Investment Management](https://www.fidelity.com/wealth/investment-management)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [News & Research]()

- [News](https://www.fidelity.com/news/overview)

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights)

- [Watchlist](https://digital.fidelity.com/ftgw/digital/watwebex)

- [Alerts](https://alertable.fidelity.com/ftgw/digital/alerts)

- [Stocks, ETFs, Crypto](https://digital.fidelity.com/prgw/digital/research/src)

- [Mutual Funds](https://fundresearch.fidelity.com/fund-screener)

- [Fixed Income, Bonds & CDs](https://fixedincome.fidelity.com/ftgw/fi/FILanding)

- [Options](https://digital.fidelity.com/ftgw/digital/options-home/)

- [IPOs](https://brokerage.fidelity.com/ftgw/brkg/ipo/calendar)

- [Annuities](https://fundresearch.fidelity.com/fund-screener/annuities/)

- [Learn](https://www.fidelity.com/learning-center/overview)

## Learn

- [Learn](https://www.fidelity.com/learning-center/overview)

- [Favorites](https://www.fidelity.com/learning-center/favorites)

- Topics

- Financial essentials

- [Saving and budgeting money](https://www.fidelity.com/learning-center/personal-finance/saving-and-budgeting-money "Saving and budgeting money")

- [Managing debt](https://www.fidelity.com/learning-center/personal-finance/managing-debt "Managing debt")

- [Saving for retirement](https://www.fidelity.com/learning-center/personal-finance/retirement/saving-for-retirement "Saving for retirement")

- [Working and income](https://www.fidelity.com/learning-center/personal-finance/working-and-income "Working and income")

- [Managing health care](https://www.fidelity.com/learning-center/personal-finance/managing-health-care "Managing health care")

- [Talking to family about money](https://www.fidelity.com/learning-center/personal-finance/talking-to-family-about-money "Talking to family about money")

- [Personal finance for students](https://www.fidelity.com/learning-center/personal-finance/personal-finance-for-students "Personal finance for students")

- [Managing taxes](https://www.fidelity.com/learning-center/personal-finance/managing-taxes/managing-taxes "Managing taxes")

- [Managing estate planning](https://www.fidelity.com/learning-center/personal-finance/managing-estate-planning "Managing estate planning")

- [Making charitable donations](https://www.fidelity.com/learning-center/personal-finance/charitable-giving/making-charitable-donations "Making charitable donations")

- Life events

- [Changing jobs](https://www.fidelity.com/learning-center/life-events/career-planning "Changing jobs")

- [Planning for college](https://www.fidelity.com/learning-center/life-events/prepare-for-college "Planning for college")

- [Getting divorced](https://www.fidelity.com/learning-center/life-events/getting-divorced "Getting divorced")

- [Becoming a parent](https://www.fidelity.com/learning-center/life-events/parenting "Becoming a parent")

- [Caring for aging loved ones](https://www.fidelity.com/learning-center/life-events/caring-for-the-aging "Caring for aging loved ones")

- [Marriage and partnering](https://www.fidelity.com/learning-center/life-events/marriage "Marriage and partnering")

- [Buying or selling a house](https://www.fidelity.com/learning-center/life-events/selling-and-buying-house "Buying or selling a house")

- [Retiring](https://www.fidelity.com/learning-center/personal-finance/retirement/planning-your-retirement "Retiring")

- [Losing a loved one](https://www.fidelity.com/learning-center/life-events/loss-of-loved-one "Losing a loved one")

- [Making a major purchase](https://www.fidelity.com/learning-center/life-events/major-purchase "Making a major purchase	")

- [Experiencing illness or injury](https://www.fidelity.com/learning-center/life-events/injury-and-illness "Experiencing illness or injury")

- [Disabilities and special needs](https://www.fidelity.com/learning-center/life-events/disabilities-and-special-needs "Disabilities and special needs")

- [Aging well](https://www.fidelity.com/learning-center/life-events/aging-well "Aging well")

- [Becoming self-employed](https://www.fidelity.com/learning-center/life-events/how-to-become-self-employed "Becoming self-employed")

- Investing and trading

- [Investing for beginners](https://www.fidelity.com/learning-center/trading-investing/investing-for-beginners "Investing for beginners")

- [Trading for beginners](https://www.fidelity.com/learning-center/trading-investing/trading-for-beginners "Trading for beginners")

- [Crypto basics](https://www.fidelity.com/learning-center/trading-investing/crypto/crypto-for-beginners "Crypto basics")

- [Crypto: Beyond the basics](https://www.fidelity.com/learning-center/trading-investing/crypto/crypto-advanced "Crypto: Beyond the basics")

- [Alternative investing](https://www.fidelity.com/learning-center/trading-investing/alternative-investing "Alternative investing")

- [Exploring stocks and sectors](https://www.fidelity.com/learning-center/trading-investing/finding-stocks-and-sector-ideas "Exploring stocks and sectors")

- [Investing for income](https://www.fidelity.com/learning-center/trading-investing/investing-for-income "Investing for income")

- [Analyzing stock fundamentals](https://www.fidelity.com/learning-center/trading-investing/fundamental-analysis/analyzing-stock-fundamentals "Analyzing stock fundamentals")

- [Using technical analysis](https://www.fidelity.com/learning-center/trading-investing/technical-analysis/using-technical-analysis "Using technical analysis")

- Investment products

- [ETFs](https://www.fidelity.com/learning-center/investment-products/etf/etfs "ETFs")

- [Mutual funds](https://www.fidelity.com/learning-center/investment-products/mutual-funds/mutual-funds "Mutual funds ")

- [Stocks](https://www.fidelity.com/learning-center/investment-products/stocks/stocks "Stocks")

- [Fixed income, bonds, CDs](https://www.fidelity.com/learning-center/investment-products/fixed-income-bonds/fixed-income-bonds-cds "Fixed income, bonds, CDs")

- [Annuities](https://www.fidelity.com/learning-center/investment-products/annuities "Annuities")

- [Closed-end funds](https://www.fidelity.com/learning-center/investment-products/closed-end-funds/closed-end-funds "Closed-end funds")

- Advanced trading

- [Using margin](https://www.fidelity.com/learning-center/trading-investing/using-margin "Using margin")

- [Options trading basics](https://www.fidelity.com/learning-center/investment-products/options/options-for-beginners "Options trading basics")

- [Options: Beyond the basics](https://www.fidelity.com/learning-center/investment-products/options/options "Options: Beyond the basics")

- [Advanced trading strategies](https://www.fidelity.com/learning-center/trading-investing/more-trading-strategies "Advanced trading strategies")

- [Using Fidelity Trader+](https://www.fidelity.com/learning-center/trading-investing/trading-platforms/using-trader-plus "Using Fidelity Trader+")

- [Options Strategy Guide](https://www.fidelity.com/learning-center/investment-products/options/options-strategy-guide/overview "Options Strategy Guide")

- [Technical Indicator Guide](https://www.fidelity.com/learning-center/trading-investing/technical-analysis/technical-indicator-guide/overview "Technical Indicator Guide")

- [Latest Market Insights](https://www.fidelity.com/viewpoints/market-and-economic-insights/market-volatility-overview "Latest Market Insights")

- [Viewpoints: Expert insights](https://www.fidelity.com/learning-center/viewpoints "Viewpoints: Expert insights")

- [Smart Money: Tips and tactics](https://www.fidelity.com/learning-center/smart-money "Smart Money: Tips and tactics")

- [Money Unscripted](https://www.fidelity.com/learning-center/money-unscripted "Money Unscripted")

- [The Trading Post](https://www.fidelity.com/learning-center/trading-post "The Trading Post")

- [Women Talk Money](https://www.fidelity.com/learning-center/women-talk-money "Women Talk Money")

- [Wealth Management Insights](https://www.fidelity.com/learning-center/wealth-management-insights "Wealth Management Insights")

- Events

- [Upcoming events](https://fidelityevents.com/allevents/special "Upcoming events")

- [On-demand webinars](https://www.fidelity.com/learning-center/events/investing-webinars "On-demand webinars")

- [Market briefings](https://fidelityevents.com/allevents/filtered?hubFilter=tags|Coaching,Market%20Analysis#hub "Market briefings")

- [Market Sense](https://www.fidelity.com/learning-center/live-pi "Market Sense")

- [Trading Strategy Desk® coaching](https://www.fidelity.com/learning-center/events/coaching-sessions "Trading Strategy Desk® coaching")

- [Trading Strategy Desk® classes](https://www.fidelity.com/learning-center/events/virtual-classrooms "Trading Strategy Desk® classes")

- Search

March 20, 2025

7 min

Save

Close Popover

***

Great, you have saved this article to you My Learn Profile page.

Share

Close Popover

***

After-tax 401(k) contributions \| Retirement benefits \| Fidelity

Clicking a link will open a new window.

- [Facebook](https://www.fidelity.com/viewpoints/retirement/401k-contributions#facebook)

- [Twitter](https://www.fidelity.com/viewpoints/retirement/401k-contributions#twitter)

- [LinkedIn](https://www.fidelity.com/viewpoints/retirement/401k-contributions#linkedin)

[Print ](https://www.fidelity.com/viewpoints/retirement/401k-contributions#print)

# What to do with after-tax 401(k) contributions

This strategy could make it worthwhile to keep saving above the annual limit.

Fidelity Viewpoints

### Key takeaways

- After contributing up to the annual limit in your 401(k), you may be able to save even more on an after-tax basis if your plan allows.

- Earnings on after-tax contributions are considered pre-tax and would grow tax-deferred until withdrawals begin.

- Converting after-tax 401(k) contributions to a Roth account is an option. After converting to a Roth, earnings can grow and be distributed tax-free if certain requirements are met.

You already know about the benefits of saving in your workplace savings plan, like a 401(k). But you may be able to save more than you think—for many people, the annual contribution limit isn't the end of their tax-advantaged saving opportunities.

In 2025, you can contribute up to \$23,500 to your 401(k). Your contributions can be entirely pre-tax or Roth (if your plan allows for Roth contributions), or some combination of the two. If you're at least age 50 by the end of the calendar year, you can add a catch-up contribution of \$7,500 pre-tax. And if you're between ages 60 and 63, you will be eligible to contribute up to \$11,250 as a catch-up contribution, if your plan allows.

Unlike Roth IRAs, there are no income caps on Roth contributions in a workplace savings account like a 401(k). Once you see that you will max out your contributions, you may want to consider making after-tax contributions if your plan allows. These are a third type of contribution to your workplace savings plan, in addition to pre-tax and Roth.

One quick note about after-tax contributions—you may not have to wait until you’ve hit the annual contribution limit during the year to make them. After-tax contributions can be made at the same time as your regular contributions—just be sure that your after-tax contributions aren't set so high that they will prevent you from fully making pre-tax and Roth contributions first. Check with your plan administrator if the rules seem unclear.

Be aware also that there is an annual maximum limit on contributions from all sources—including your employer. As you’re calculating the amount you can contribute, include any matching or profit sharing/non-elective contributions from your employer so that “free money” contribution doesn’t get crowded out.

The IRS allows a total of up to \$70,000 of employer and employee contributions to be saved in a 401(k) for 2025, plus any age-dependent employee catch-up contributions. Here's what's included:

**What you save**

- Elective deferrals (either tax-deferred, Roth, or a combination)

- Optional after-tax contributions to your workplace savings plan beyond the annual elective deferral limit (if allowed by your employer)

**What your employer can contribute on your behalf**

- Employer matching contributions

- Employer nonelective contributions, typically profit sharing

Sign up for *Fidelity Viewpoints* weekly email for our latest insights.

[Subscribe now](https://www.fidelity.com/viewpoints/retirement/401k-contributions#subscribe-container)

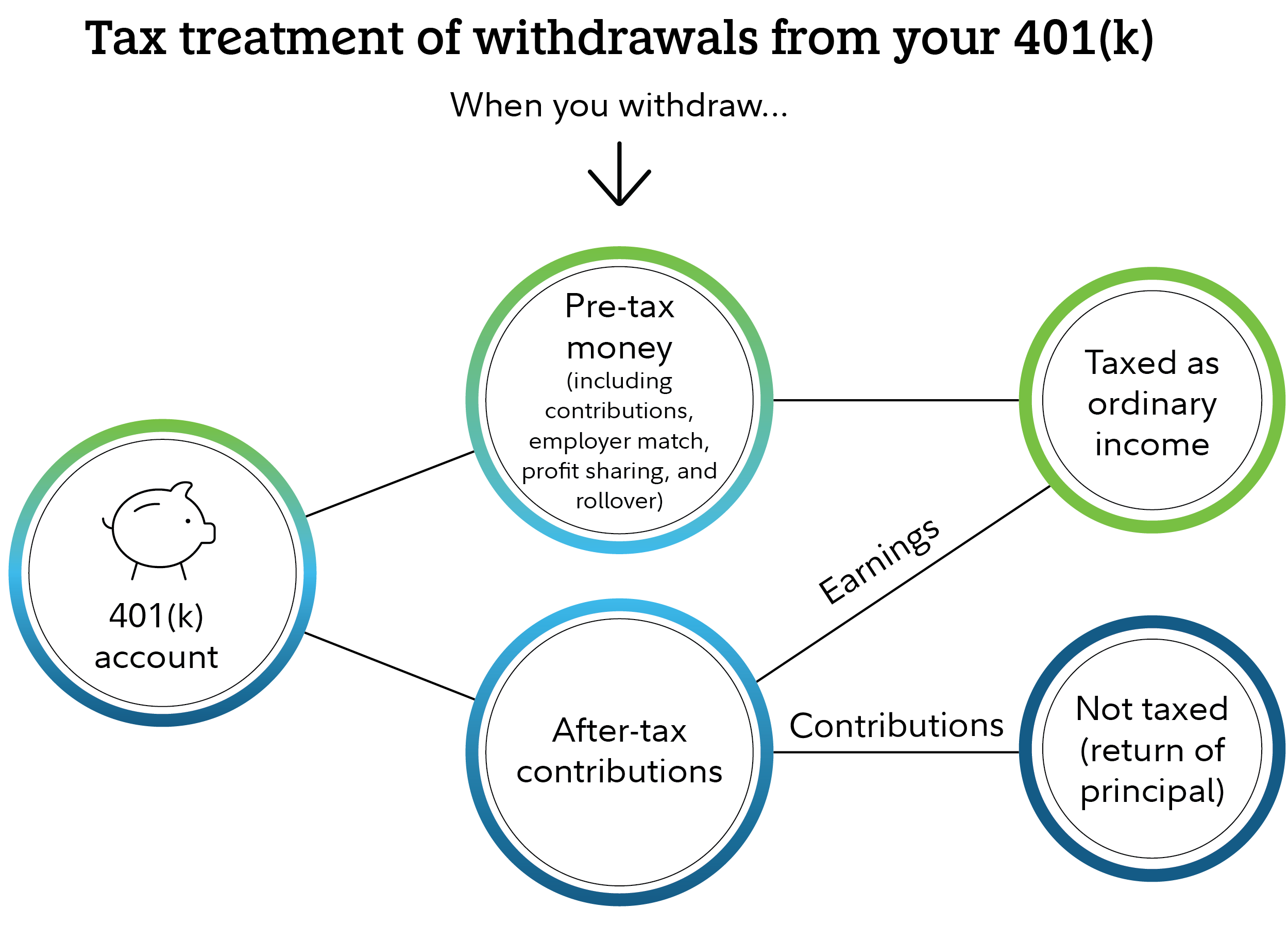

After-tax contributions to your workplace plan can be withdrawn without taxes or penalties. Any earnings on those after-tax contributions are considered pre-tax balances—so taxes would have to be paid on withdrawals of the earnings and there may be a 10% penalty if you're under age 59½.

What you should know is that you won't be able to withdraw your after-tax contributions without also withdrawing any earnings associated with them. Taking out just the after-tax balance would not be allowed (unless they are rolled over to an IRA).

Let's say you made \$10,000 in after-tax contributions and that money earned \$2,000 in returns. In order to withdraw the \$10,000, the \$2,000 in earnings would need to be withdrawn as well. And that applies if you are converting the after-tax balance as well (if you are converting in-plan).

With respect to federal taxation only. Distributions may or may not be subject to state taxation.

### Potential strategies for after-tax 401(k) contributions

Making after-tax contributions allows you to invest more money with the potential for tax-deferred growth. That's a powerful benefit on its own—but that's not the end of the story. You could then go a step further and convert your after-tax contributions to a Roth account. There are a couple of different ways to accomplish that (if your employer permits), including rolling over your balances to an IRA or doing an in-plan conversion if it's offered by your employer along with a Roth option.

When you convert after-tax balances to Roth, no taxes would be due on the conversion of your contributions. However, when you convert, you have to include associated earnings, which would be subject to tax. So, if the option is available to you, you may want to roll those earnings to a traditional IRA instead. That strategy is covered more in subsequent sections.

Earnings in a Roth account grow and may potentially be distributed tax-free as long as certain conditions are met. So no taxes would be due on withdrawals—as long as they take place after age 59½ and the [5-year aging requirement](https://www.fidelity.com/learning-center/personal-finance/retirement/roth-ira-5-year-rule) has been met.

Satisfying the 5-year aging requirement for the tax-free withdrawal of earnings means that there are at least 5 years between either the year of your first Roth contribution or the year the conversion took place and any withdrawals. The 5-year clock starts on January 1 of the tax year in which the conversion occurred or the contribution was made, no matter when during the year it actually happened. So if you converted in December, the aging requirement might, in practice, be only a bit more than 4 years.

Not all employers offer a Roth option in their retirement plan—or they may not offer the option to do an in-plan conversion. If your employer does not offer a Roth option or the in-plan Roth conversion feature, you can still roll over your after-tax contributions to a Roth IRA. Here are the 3 strategies. The options available to you will depend on your situation.

### 1\. In-plan Roth conversion

Many employers do offer a Roth option in their retirement plan. And some plans allow you to do an in-plan conversion.

An in-plan Roth conversion allows you to take after-tax contributions and convert them to Roth. Some employers even offer an auto-convert feature inside their plan. You can set it up so that any after-tax contributions are automatically converted to a Roth at regular intervals. Though after-tax contributions have already been taxed, any earnings associated with them have not—so converting earnings will trigger a tax bill in the year of the conversion.

### 2\. Rolling out to IRAs after an in-plan conversion

After completing a Roth conversion within your workplace retirement plan, rolling out to IRAs should be relatively straightforward if you choose to do that. If you’re planning to roll the money out to a Roth IRA at some point and don’t already contribute to a Roth IRA, it may make sense to open an account and make at least one contribution now, if possible, so the 5-year clock starts ticking on this account. Roth 401(k)s have a 5-year aging requirement as well that is tracked separately from Roth IRAs. These rules don't need to be subsequently met again in the future, unlike Roth conversions, which have a new 5-year clock for each converted amount (however, the earnings follow the rule for either the plan or the Roth IRA).

If you earn too much to contribute to a Roth IRA, you do have options. Read *Viewpoints* on Fidelity.com: [Do you earn too much for a Roth IRA?](https://www.fidelity.com/viewpoints/retirement/earn-too-much-contribute-Roth-IRA-conversion)

### 3\. IRA rollover without an in-plan conversion

You can roll over after-tax contributions to a Roth IRA, and it is possible to do that before age 59½. There is a big catch, though: Not all plans allow withdrawals while you’re still with the company, and your retirement plan may have some rules around the requirements for rolling out of the plan. In-service withdrawals come with some potentially complicated rules, so it’s important to understand the rules the IRS has and those of your retirement plan.

In general, to roll after-tax money to a Roth IRA, earnings on the after-tax balance must, in most cases, also be withdrawn. You may have a few options.

If you have both pre-tax and after-tax contributions, you may be able to take a partial distribution from your retirement plan, consisting of just one or the other, if the plan separately tracks the sources of all of your contributions. In that case, you may want to roll out only the after-tax source balances directly into a Roth IRA.

The pre-tax contributions, along with the earnings from both the pre-tax and the after-tax contributions, can be rolled to a traditional IRA, incurring no current income tax.

Alternatively, you can roll everything into a Roth IRA, but you would need to pay income taxes on the pre-tax contributions and all of the earnings.

Important note: Any partial withdrawals or in-plan conversions may affect eligibility for [net unrealized appreciation](https://www.fidelity.com/learning-center/personal-finance/retirement/company-stock) treatment on appreciated employer stock held in the plan.

It's advisable to consult with a financial advisor before making any decisions.

To find out more, read *Viewpoints* on Fidelity.com: [Rolling after-tax money in a 401(k) to a Roth IRA](https://www.fidelity.com/viewpoints/retirement/IRS-401k-rollover-guidance)

### Be sure to consider all your options

Making after-tax contributions and then converting to Roth may seem complicated, but the long-term benefits can make it worthwhile. But bear in mind: there can be benefits to keeping your money in the workplace savings plan. Balances in your workplace retirement account may be available for loans, if your plan allows them, while balances in an IRA are not. On the other hand, IRAs have certain advantages as well. For instance, you may be able to get a broader range of investment choices. So it's a good idea to check with your financial advisor and tax advisor before choosing a strategy.

## Tax-free retirement income? Sounds good.

A Roth IRA can be a powerful way to save for retirement since potential earnings grow tax-free.

[Learn more](https://www.fidelity.com/retirement-ira/roth-ira)

## More to explore

### [Explore Roth IRA conversions](https://www.fidelity.com/building-savings/learn-about-iras/convert-to-roth)

Know how to take advantage of the potential of a Roth IRA.

### [Get help with your plan](https://www.fidelity.com/calculators-tools/planning-guidance-center)

Create a retirement income plan in our Planning & Guidance Center.

## Subscribe to *Fidelity Viewpoints®*

Timely news and insights from our pros on markets, investing, and personal finance.(debug tcm:2365-349569)

### Looking for more ideas and insights?

We'll deliver them right to your inbox.

Manage subscriptions

### Thanks for subscribing\!

Check out your Favorites page, where you can:

- Tell us the topics you want to learn more about

- View content you've saved for later

- Subscribe to our newsletters

[Go to Favorites](https://www.fidelity.com/learning-center/favorites)

### We're on our way, but not quite there yet

Good news, you're on the early-access list.

But we're not available in your state just yet. As soon as we are, we'll let you know. In the meantime, boost your crypto brainpower in our Learning Center.

Manage subscriptions

### Oh, hello again\!

Good news, you’re already on the early-access list. Keep an eye on your email for your invitation to Fidelity Crypto.

Manage subscriptions

Close dialog

### Thanks for subscribing to Looking for more ideas and insights? You might like these too:

### Looking for more ideas and insights? You might like these too:

### *Fidelity Viewpoints®*

Timely news and insights from our pros on markets, investing, and personal finance.(debug tcm:2 ...

### Decode Crypto

Clarity on crypto every month. Build your knowledge with education for all levels.

### *Fidelity Smart Money℠*

What the news means for your money, plus tips to help you spend, save, and invest.

### Active Investor

Our most advanced investment insights, strategies, and tools.

### *Insights from Fidelity Wealth Management* ℠

Timely news, events, and wealth strategies from top Fidelity thought leaders.

### Women Talk Money

Real talk and helpful tips about money, investing, and careers.

### Educational Webinars and Events

Free financial education from Fidelity and other leading industry professionals.

*Fidelity Viewpoints®*

Timely news and insights from our pros on markets, investing, and personal finance.(debug tcm:2 ...

Decode Crypto

Clarity on crypto every month. Build your knowledge with education for all levels.

*Fidelity Smart Money℠*

What the news means for your money, plus tips to help you spend, save, and invest.

Active Investor

Our most advanced investment insights, strategies, and tools.

*Insights from Fidelity Wealth Management* ℠

Timely news, events, and wealth strategies from top Fidelity thought leaders.

Women Talk Money

Real talk and helpful tips about money, investing, and careers.

Educational Webinars and Events

Free financial education from Fidelity and other leading industry professionals.

Done

Add subscriptions

No, thanks.

Loading

- [Managing taxes](https://www.fidelity.com/learning-center/personal-finance/managing-taxes/managing-taxes)

- [Changing jobs](https://www.fidelity.com/learning-center/life-events/career-planning)

- [Investing for income](https://www.fidelity.com/learning-center/trading-investing/investing-for-income)

- [Preparing for retirement](https://www.fidelity.com/learning-center/personal-finance/retirement/planning-your-retirement)

- [Saving for retirement](https://www.fidelity.com/learning-center/personal-finance/retirement/saving-for-retirement)

- [Living in retirement](https://www.fidelity.com/learning-center/personal-finance/retirement/planning-your-retirement)

- [Trading options](https://www.fidelity.com/learning-center/investment-products/options/options)

For a distribution to be considered qualified, the 5-year aging requirement has to be satisfied, and you must be age 59½ or older or meet one of several exemptions (disability, qualified first-time home purchase, or death among them).

For tax year 2025, if you're single, the ability to contribute to a Roth IRA begins to phase out at MAGI of \$150,000 and is completely phased out at \$165,000. If you're married filing jointly, the phaseout range is \$236,000 to \$246,000.

**Be sure to consider all your available options and the applicable fees and features of each before moving your retirement assets.**

Fidelity does not provide legal or tax advice. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results. Fidelity cannot guarantee that the information herein is accurate, complete, or timely. Fidelity makes no warranties with regard to such information or results obtained by its use, and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Consult an attorney or tax professional regarding your specific situation.

Fidelity Brokerage Services LLC, Member NYSE, [SIPC](https://www.sipc.org/), 900 Salem Street, Smithfield, RI 02917

888539\.9.0

- [Mutual Funds](https://www.fidelity.com/mutual-funds/overview)

- [ETFs](https://www.fidelity.com/etfs/overview)

- [Fixed Income](https://www.fidelity.com/fixed-income-bonds/overview)

- [Bonds](https://www.fidelity.com/fixed-income-bonds/individual-bonds/overview)

- [CDs](https://www.fidelity.com/fixed-income-bonds/cds)

- [Options](https://www.fidelity.com/options-trading/overview)

- [Crypto](https://www.fidelity.com/crypto/overview)

- [Fidelity Trader+](https://www.fidelity.com/trading/trading-platforms)

- [Investor Centers](https://www.fidelity.com/branches/branch-locations)

- [Stocks](https://www.fidelity.com/stock-trading/overview)

- [Online Trading](https://www.fidelity.com/trading/overview)

- [Direct Indexing](https://www.fidelity.com/direct-indexing/overview)

- [Sustainable Investing](https://www.fidelity.com/sustainable/overview)

- [Annuities](https://www.fidelity.com/annuities/overview)

- [Life Insurance](https://www.fidelity.com/life-insurance/term-life-insurance/overview)

- [Long-Term Care Planning](https://www.fidelity.com/life-insurance/long-term-care/overview)

- [529 Plans](https://www.fidelity.com/529-plans/overview)

- [Health Savings Account](https://www.fidelity.com/go/hsa/why-hsa)

- [IRAs](https://www.fidelity.com/retirement/retirement-accounts)

- [Retirement Planning](https://www.fidelity.com/retirement/retirement-planning)

- [Small Business Retirement Plans](https://www.fidelity.com/retirement-ira/small-business/compare-retirement-plans)

- [Charitable Giving](https://www.fidelity.com/building-savings/charity-and-philanthropy)

- [Marketplace Solutions](https://www.fidelity.com/go/marketplace/overview)

- [FINRA's BrokerCheck, (Opens in a new window)](https://brokercheck.finra.org/Firm/Summary/7784)

- [Why Fidelity](https://www.fidelity.com/why-fidelity/overview)

### Stay Connected

The search input box here

-  [Instagram, (Opens in a new window)](https://www.instagram.com/fidelityinvestments)

-  [LinkedIn, (Opens in a new window)](https://www.linkedin.com/company/fidelity-investments)

-  [YouTube, (Opens in a new window)](https://www.youtube.com/user/fidelityinvestments)

-  [Reddit, (Opens in a new window)](https://www.reddit.com/r/fidelityinvestments/)

-  [X (Twitter), (Opens in a new window)](https://www.twitter.com/fidelity)

-  [Facebook, (Opens in a new window)](https://www.facebook.com/fidelityinvestments)

-  [TikTok, (Opens in a new window)](https://www.tiktok.com/@fidelityinvestments)

-  [Discord, (Opens in a new window)](https://discord.gg/FidelityInvestments)

-  [Fidelity Apps](https://www.fidelity.com/mobile/overview)

-  [Refer a Friend](https://www.fidelity.com/customer-service/friendsandfamily3a?ccsource=RAFFooterNav)

- [Careers](https://jobs.fidelity.com/)

- [News Releases](https://newsroom.fidelity.com/)

- [About Fidelity](https://about.fidelity.com/)

- [International](https://www.fidelityinternational.com/)

Copyright 1998-2026 FMR LLC. All Rights Reserved.

- [Terms of Use](https://www.fidelity.com/terms-of-use)

- [Privacy](https://www.fidelity.com/privacy/overview)

- [Security](https://www.fidelity.com/security/overview)

- [Site Map](https://www.fidelity.com/sitemap/overview)

- [Accessibility](https://www.fidelity.com/accessibility/overview)

- [Contact Us](https://www.fidelity.com/customer-service/contact-us) , (Opens in a new window)

- [Share Your Screen](https://www.fidelity.com/viewpoints/retirement/401k-contributions)

- [Disclosures](https://communications.fidelity.com/information/crs/) , (Opens in a new window)

- [Manage My Targeting/Advertising Cookies](https://www.fidelity.com/viewpoints/retirement/401k-contributions)

[This is for persons in the US only.](https://www.fidelity.com/terms-of-use#For)

Privacy Settings

When you visit our website, it may store or retrieve information on your browser, mostly in the form of cookies. Because we respect your right to privacy, you can choose not to allow some types of cookies. Click on the different category headings to find out more and change our default settings. However, blocking some types of cookies may impact your experience on this site and the services we are able to offer.

***

Strictly Necessary Cookies

These cookies are necessary for this website to function and cannot be switched off in our systems. You can set your browser to block or alert you about these cookies, but if you block these cookies, some parts of the site will not work. These cookies do not store any personally identifiable information.

***

Performance Cookies

These cookies allow us to count visits and traffic sources so we can measure and improve the performance of our site. They help us to know which pages are the most and least popular and see how visitors move around the site. All information these cookies collect is aggregated and therefore anonymous. If you do not allow these cookies we will not know when you have visited our site, and will not be able to monitor its performance.

***

Functional Cookies

These cookies enable the website to provide enhanced functionality and personalization. They may be set by us or by third party providers whose services we have added to our pages. If you do not allow these cookies then some or all of these services may not function properly.

***

Targeting or Advertising Cookies

These cookies help us present relevant online advertising and marketing messages to you, and measure the effectiveness of our advertising and marketing campaigns. These cookies may be placed on your device by us or by our third-party advertising providers. When these cookies have been placed on your device, they can be recognized by certain advertising platforms used by other websites you visit, and this allows us to present our advertisements to you on those third party websites. While targeting cookies can identify you when you visit different websites, the information collected is anonymous. They do not store personal information, but are based on uniquely identifying your browser and device. If you do not allow these cookies, our online advertisements that you see may be less relevant to you.

***

Cancel

Save

Close dialog

##

close virtual assistant

close Fidelity Virtual Assistant menu

## Menu

- Important Information

Welcome to the Fidelity Assistant\!

Start typing and we'll suggest a few topics for you. You can also enter a simple question or phrase, and we'll offer our best answer.

Ready? Let's get started.

[Important information](https://www.fidelity.com/viewpoints/retirement/401k-contributions)

To get your conversation started, type a question in the entry field or choose from one of the following popular topics and commonly asked questions.

- How can I change my retirement contribution?

- What strategies can I implement to improve my retirement savings contributions?

- Can after-tax contributions be made to a retirement plan that does not allow them?

Provide Feedback

answers will appear above the text input

Submit message |

| Readable Markdown | What to do with after-tax 401(k) contributions

This strategy could make it worthwhile to keep saving above the annual limit.

### Key takeaways

- After contributing up to the annual limit in your 401(k), you may be able to save even more on an after-tax basis if your plan allows.

- Earnings on after-tax contributions are considered pre-tax and would grow tax-deferred until withdrawals begin.

- Converting after-tax 401(k) contributions to a Roth account is an option. After converting to a Roth, earnings can grow and be distributed tax-free if certain requirements are met.

You already know about the benefits of saving in your workplace savings plan, like a 401(k). But you may be able to save more than you think—for many people, the annual contribution limit isn't the end of their tax-advantaged saving opportunities.

In 2025, you can contribute up to \$23,500 to your 401(k). Your contributions can be entirely pre-tax or Roth (if your plan allows for Roth contributions), or some combination of the two. If you're at least age 50 by the end of the calendar year, you can add a catch-up contribution of \$7,500 pre-tax. And if you're between ages 60 and 63, you will be eligible to contribute up to \$11,250 as a catch-up contribution, if your plan allows.

Unlike Roth IRAs, there are no income caps on Roth contributions in a workplace savings account like a 401(k). Once you see that you will max out your contributions, you may want to consider making after-tax contributions if your plan allows. These are a third type of contribution to your workplace savings plan, in addition to pre-tax and Roth.

One quick note about after-tax contributions—you may not have to wait until you’ve hit the annual contribution limit during the year to make them. After-tax contributions can be made at the same time as your regular contributions—just be sure that your after-tax contributions aren't set so high that they will prevent you from fully making pre-tax and Roth contributions first. Check with your plan administrator if the rules seem unclear.

Be aware also that there is an annual maximum limit on contributions from all sources—including your employer. As you’re calculating the amount you can contribute, include any matching or profit sharing/non-elective contributions from your employer so that “free money” contribution doesn’t get crowded out.

The IRS allows a total of up to \$70,000 of employer and employee contributions to be saved in a 401(k) for 2025, plus any age-dependent employee catch-up contributions. Here's what's included:

**What you save**

- Elective deferrals (either tax-deferred, Roth, or a combination)

- Optional after-tax contributions to your workplace savings plan beyond the annual elective deferral limit (if allowed by your employer)

**What your employer can contribute on your behalf**

- Employer matching contributions

- Employer nonelective contributions, typically profit sharing

Sign up for *Fidelity Viewpoints* weekly email for our latest insights.

After-tax contributions to your workplace plan can be withdrawn without taxes or penalties. Any earnings on those after-tax contributions are considered pre-tax balances—so taxes would have to be paid on withdrawals of the earnings and there may be a 10% penalty if you're under age 59½.

What you should know is that you won't be able to withdraw your after-tax contributions without also withdrawing any earnings associated with them. Taking out just the after-tax balance would not be allowed (unless they are rolled over to an IRA).

Let's say you made \$10,000 in after-tax contributions and that money earned \$2,000 in returns. In order to withdraw the \$10,000, the \$2,000 in earnings would need to be withdrawn as well. And that applies if you are converting the after-tax balance as well (if you are converting in-plan).

With respect to federal taxation only. Distributions may or may not be subject to state taxation.

### Potential strategies for after-tax 401(k) contributions

Making after-tax contributions allows you to invest more money with the potential for tax-deferred growth. That's a powerful benefit on its own—but that's not the end of the story. You could then go a step further and convert your after-tax contributions to a Roth account. There are a couple of different ways to accomplish that (if your employer permits), including rolling over your balances to an IRA or doing an in-plan conversion if it's offered by your employer along with a Roth option.

When you convert after-tax balances to Roth, no taxes would be due on the conversion of your contributions. However, when you convert, you have to include associated earnings, which would be subject to tax. So, if the option is available to you, you may want to roll those earnings to a traditional IRA instead. That strategy is covered more in subsequent sections.

Earnings in a Roth account grow and may potentially be distributed tax-free as long as certain conditions are met. So no taxes would be due on withdrawals—as long as they take place after age 59½ and the [5-year aging requirement](https://www.fidelity.com/learning-center/personal-finance/retirement/roth-ira-5-year-rule) has been met.

Satisfying the 5-year aging requirement for the tax-free withdrawal of earnings means that there are at least 5 years between either the year of your first Roth contribution or the year the conversion took place and any withdrawals. The 5-year clock starts on January 1 of the tax year in which the conversion occurred or the contribution was made, no matter when during the year it actually happened. So if you converted in December, the aging requirement might, in practice, be only a bit more than 4 years.

Not all employers offer a Roth option in their retirement plan—or they may not offer the option to do an in-plan conversion. If your employer does not offer a Roth option or the in-plan Roth conversion feature, you can still roll over your after-tax contributions to a Roth IRA. Here are the 3 strategies. The options available to you will depend on your situation.

### 1\. In-plan Roth conversion

Many employers do offer a Roth option in their retirement plan. And some plans allow you to do an in-plan conversion.

An in-plan Roth conversion allows you to take after-tax contributions and convert them to Roth. Some employers even offer an auto-convert feature inside their plan. You can set it up so that any after-tax contributions are automatically converted to a Roth at regular intervals. Though after-tax contributions have already been taxed, any earnings associated with them have not—so converting earnings will trigger a tax bill in the year of the conversion.

### 2\. Rolling out to IRAs after an in-plan conversion

After completing a Roth conversion within your workplace retirement plan, rolling out to IRAs should be relatively straightforward if you choose to do that. If you’re planning to roll the money out to a Roth IRA at some point and don’t already contribute to a Roth IRA, it may make sense to open an account and make at least one contribution now, if possible, so the 5-year clock starts ticking on this account. Roth 401(k)s have a 5-year aging requirement as well that is tracked separately from Roth IRAs. These rules don't need to be subsequently met again in the future, unlike Roth conversions, which have a new 5-year clock for each converted amount (however, the earnings follow the rule for either the plan or the Roth IRA).

If you earn too much to contribute to a Roth IRA, you do have options. Read *Viewpoints* on Fidelity.com: [Do you earn too much for a Roth IRA?](https://www.fidelity.com/viewpoints/retirement/earn-too-much-contribute-Roth-IRA-conversion)

### 3\. IRA rollover without an in-plan conversion

You can roll over after-tax contributions to a Roth IRA, and it is possible to do that before age 59½. There is a big catch, though: Not all plans allow withdrawals while you’re still with the company, and your retirement plan may have some rules around the requirements for rolling out of the plan. In-service withdrawals come with some potentially complicated rules, so it’s important to understand the rules the IRS has and those of your retirement plan.

In general, to roll after-tax money to a Roth IRA, earnings on the after-tax balance must, in most cases, also be withdrawn. You may have a few options.

If you have both pre-tax and after-tax contributions, you may be able to take a partial distribution from your retirement plan, consisting of just one or the other, if the plan separately tracks the sources of all of your contributions. In that case, you may want to roll out only the after-tax source balances directly into a Roth IRA.

The pre-tax contributions, along with the earnings from both the pre-tax and the after-tax contributions, can be rolled to a traditional IRA, incurring no current income tax.

Alternatively, you can roll everything into a Roth IRA, but you would need to pay income taxes on the pre-tax contributions and all of the earnings.

Important note: Any partial withdrawals or in-plan conversions may affect eligibility for [net unrealized appreciation](https://www.fidelity.com/learning-center/personal-finance/retirement/company-stock) treatment on appreciated employer stock held in the plan.

It's advisable to consult with a financial advisor before making any decisions.

To find out more, read *Viewpoints* on Fidelity.com: [Rolling after-tax money in a 401(k) to a Roth IRA](https://www.fidelity.com/viewpoints/retirement/IRS-401k-rollover-guidance)

### Be sure to consider all your options

Making after-tax contributions and then converting to Roth may seem complicated, but the long-term benefits can make it worthwhile. But bear in mind: there can be benefits to keeping your money in the workplace savings plan. Balances in your workplace retirement account may be available for loans, if your plan allows them, while balances in an IRA are not. On the other hand, IRAs have certain advantages as well. For instance, you may be able to get a broader range of investment choices. So it's a good idea to check with your financial advisor and tax advisor before choosing a strategy. |

| Shard | 93 (laksa) |

| Root Hash | 17952695050214760493 |

| Unparsed URL | com,fidelity!www,/viewpoints/retirement/401k-contributions s443 |