ℹ️ Skipped - page is already crawled

| Filter | Status | Condition | Details |

|---|---|---|---|

| HTTP status | PASS | download_http_code = 200 | HTTP 200 |

| Age cutoff | PASS | download_stamp > now() - 6 MONTH | 0.5 months ago |

| History drop | PASS | isNull(history_drop_reason) | No drop reason |

| Spam/ban | PASS | fh_dont_index != 1 AND ml_spam_score = 0 | ml_spam_score=0 |

| Canonical | PASS | meta_canonical IS NULL OR = '' OR = src_unparsed | Not set |

| Property | Value |

|---|---|

| URL | https://breakingdownfinance.com/finance-topics/risk-management/realized-volatility/ |

| Last Crawled | 2026-04-07 21:15:35 (15 days ago) |

| First Indexed | 2018-09-28 21:23:16 (7 years ago) |

| HTTP Status Code | 200 |

| Content | |

| Meta Title | Realized Volatility - Breaking Down Finance |

| Meta Description | The realized volatility is an alternative metric to calculate the price variability. In the provided Excel sheet we show the realized volatility can be... |

| Meta Canonical | null |

| Boilerpipe Text | The realized volatility is a new rising concept in the financial literature. It is derived from the realized variance and introduced by Bandorff-Nielssen and Sheppard. It is often used to measure the price variability of intraday returns. Although it can also be used at lower data frequencies.

Realized volatility formula

In order to calculate it, you first need to calculate the log returns of the security as shown in the formula below.

In a next step, the realized volatility is calculated by taking the sum over the past

N

squared return.

The realized volatility is simply the square root of the realized variance.

Annualizing realized volatility

When having calculated the realized variance of a single day, this can be annualized in the following way. By calculating the realized variance of a single day using high frequency data, the annualized realized variance equals the daily realized variance multiplied by the amount of trading days.

The annualized realized volatility is simply the square root of the realized variance.

Summary

The realized volatility, or in general the realized variance, is a new financial volatility concept unknown to many investors. It is a popular technical to measure intraday price risk. As such it is useful to extend standard risk management practices with this approach. |

| Markdown | [](https://breakingdownfinance.com/)

- [Home](https://breakingdownfinance.com/)

- [Finance topics](https://breakingdownfinance.com/finance-topics/)

- [Finance basics](https://breakingdownfinance.com/finance-topics/finance-basics/)

- [Interest rate compounding](https://breakingdownfinance.com/finance-topics/finance-basics/interest-rate-compounding/)

- [Discounting cash flows](https://breakingdownfinance.com/finance-topics/finance-basics/discounting-cash-flows/)

- [Basic statistics](https://breakingdownfinance.com/finance-topics/finance-basics/basic-statistics-2/)

- [Return calculation](https://breakingdownfinance.com/finance-topics/finance-basics/return-calculation/)

- [Credit ratings](https://breakingdownfinance.com/finance-topics/finance-basics/credit-ratings/)

- [Bonds](https://breakingdownfinance.com/finance-topics/finance-basics/bonds/)

- [Shares](https://breakingdownfinance.com/finance-topics/finance-basics/shares/)

- [Derivatives](https://breakingdownfinance.com/finance-topics/finance-basics/derivatives/)

- [Hybrid securities](https://breakingdownfinance.com/finance-topics/finance-basics/hybrid-securities/)

- [Modern Portfolio Theory](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/)

- [Investment Diversification](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/investment-diversification/)

- [Capital Allocation Line (CAL)](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/capital-allocation-line/)

- [Modern Portfolio Theory of Markowitz](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/modern-portfolio-theory-of-markowitz/)

- [Portfolio Optimization](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/portfolio-optimization/)

- [Factor Models](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/factor-models/)

- [Treynor-Black model](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/treynor-black-model/)

- [Naive Diversification](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/naive-diversification/)

- [CAPM](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/capm/)

- [Value Averaging](https://breakingdownfinance.com/finance-topics/modern-portfolio-theory/value-averaging/)

- [Bond valuation](https://breakingdownfinance.com/finance-topics/bond-valuation/)

- [Backward Induction Bond Valuation](https://breakingdownfinance.com/finance-topics/bond-valuation/backward-induction-bond-valuation/)

- [Credit Valuation Adjustment (CVA)](https://breakingdownfinance.com/finance-topics/bond-valuation/credit-valuation-adjustment-cva/)

- [Bootstrapping Spot Rates](https://breakingdownfinance.com/finance-topics/bond-valuation/bootstrapping-spot-rates/)

- [Yield curve](https://breakingdownfinance.com/finance-topics/bond-valuation/yield-curve/)

- [Fixed rate bond valuation](https://breakingdownfinance.com/finance-topics/bond-valuation/fixed-rate-bond-valuation/)

- [Duration](https://breakingdownfinance.com/finance-topics/bond-valuation/duration/)

- [Interest rate and bond value](https://breakingdownfinance.com/finance-topics/bond-valuation/interest-rate-and-bond-value/)

- [Accrued interest](https://breakingdownfinance.com/finance-topics/bond-valuation/accrued-interest/)

- [Floating rate bond valuation](https://breakingdownfinance.com/finance-topics/bond-valuation/floating-rate-bond-valuation/)

- [Equity valuation](https://breakingdownfinance.com/finance-topics/equity-valuation/)

- [Justified Price-to-book Multiple](https://breakingdownfinance.com/finance-topics/equity-valuation/justified-price-to-book-multiple/)

- [Justified Price-to-Sales Ratio](https://breakingdownfinance.com/finance-topics/equity-valuation/justified-price-to-sales-ratio/)

- [Present Value of Growth Opportunities (PVGO)](https://breakingdownfinance.com/finance-topics/equity-valuation/present-value-of-growth-opportunities-pvgo/)

- [PEG Ratio](https://breakingdownfinance.com/finance-topics/equity-valuation/peg-ratio/)

- [Dividend Discount Model](https://breakingdownfinance.com/finance-topics/equity-valuation/dividend-discount-model/)

- [Justified PE](https://breakingdownfinance.com/finance-topics/equity-valuation/justified-pe/)

- [PE ratio](https://breakingdownfinance.com/finance-topics/equity-valuation/pe-ratio/)

- [CAPE Ratio](https://breakingdownfinance.com/finance-topics/equity-valuation/cape-ratio/)

- [Dividend yield](https://breakingdownfinance.com/finance-topics/equity-valuation/dividend-yield/)

- [Arbitrage pricing theory](https://breakingdownfinance.com/finance-topics/equity-valuation/arbitrage-pricing-theory/)

- [Derivative valuation](https://breakingdownfinance.com/finance-topics/derivative-valuation/)

- [Margin Call Price](https://breakingdownfinance.com/finance-topics/alternative-investments/margin-call-price/)

- [Forward contract](https://breakingdownfinance.com/finance-topics/derivative-valuation/forward-contract/)

- [Swap valuation](https://breakingdownfinance.com/finance-topics/derivative-valuation/swap-valuation/)

- [Option valuation](https://breakingdownfinance.com/finance-topics/derivative-valuation/option-valuation/)

- [Performance measurement](https://breakingdownfinance.com/finance-topics/performance-measurement/)

- [Manipulation Proof Performance Measure](https://breakingdownfinance.com/finance-topics/alternative-investments/manipulation-proof-performance-measure/)

- [Pastor-Stambaugh Model](https://breakingdownfinance.com/finance-topics/equity-valuation/pastor-stambaugh-model/)

- [Fung-Hsieh 7 Factor Model](https://breakingdownfinance.com/finance-topics/performance-measurement/fung-hsieh-7-factor-model/)

- [Kappa Ratio](https://breakingdownfinance.com/finance-topics/performance-measurement/kappa-ratio/)

- [Lower Partial Moment](https://breakingdownfinance.com/finance-topics/performance-measurement/lower-partial-moment/)

- [Sterling Ratio](https://breakingdownfinance.com/finance-topics/performance-measurement/sterling-ratio/)

- [Sharpe ratio](https://breakingdownfinance.com/finance-topics/performance-measurement/sharpe-ratio/)

- [Jensen’s alpha](https://breakingdownfinance.com/finance-topics/performance-measurement/jensens-alpha/)

- [Treynor Ratio](https://breakingdownfinance.com/finance-topics/performance-measurement/treynor-ratio/)

- [Day trading success rate](https://breakingdownfinance.com/finance-topics/performance-measurement/day-trading-success-rate/)

- [Risk management](https://breakingdownfinance.com/finance-topics/risk-management/)

- [Market risk](https://breakingdownfinance.com/finance-topics/risk-management/market-risk/)

- [Altman z-score](https://breakingdownfinance.com/finance-topics/risk-management/altman-z-score/)

- [Drawdown](https://breakingdownfinance.com/finance-topics/risk-management/drawdown/)

- [EWMA](https://breakingdownfinance.com/finance-topics/risk-management/ewma/)

- [Realized Volatility](https://breakingdownfinance.com/finance-topics/risk-management/realized-volatility/)

- [Behavioural Finance](https://breakingdownfinance.com/finance-topics/behavioural-finance/)

- [Prospect Theory](https://breakingdownfinance.com/finance-topics/behavioural-finance/prospect-theory/)

- [Disposition Effect](https://breakingdownfinance.com/finance-topics/behavioural-finance/disposition-effect/)

- [Other behavioral biases](https://breakingdownfinance.com/finance-topics/behavioural-finance/)

- [Passive Investing](https://breakingdownfinance.com/trading-strategies/passive-investing/)

- [ETF](https://breakingdownfinance.com/trading-strategies/passive-investing/etf/)

- [Total Expense Ratio](https://breakingdownfinance.com/trading-strategies/passive-investing/total-expense-ratio/)

- [Sector ETF](https://breakingdownfinance.com/trading-strategies/passive-investing/sector-etf/)

- [Bid Ask Spread](https://breakingdownfinance.com/trading-strategies/passive-investing/bid-ask-spread/)

- [Variance Drag](https://breakingdownfinance.com/trading-strategies/passive-investing/etf/variance-drag/)

- [Portfolio Turnover](https://breakingdownfinance.com/trading-strategies/passive-investing/portfolio-turnover/)

- [Personal finance](https://breakingdownfinance.com/trading-strategies/personal-finance/)

- [Mortgage](https://breakingdownfinance.com/trading-strategies/personal-finance/mortgage/)

- [Straight Mortgage](https://breakingdownfinance.com/trading-strategies/personal-finance/straight-mortgage/)

- [Annuity Mortgage](https://breakingdownfinance.com/trading-strategies/personal-finance/annuity-mortgage/)

- [Technical Analysis](https://breakingdownfinance.com/trading-strategies/technical-analysis/)

- [Moving Average](https://breakingdownfinance.com/trading-strategies/technical-analysis/moving-average/)

- [Exponentially Weighted Moving Average](https://breakingdownfinance.com/trading-strategies/technical-analysis/exponentially-weighted-moving-average/)

- [Ulcer Index](https://breakingdownfinance.com/finance-topics/performance-measurement/ulcer-index/)

- [Upside Potential Ratio](https://breakingdownfinance.com/finance-topics/performance-measurement/upside-potential-ratio/)

- [MACD](https://breakingdownfinance.com/trading-strategies/technical-analysis/macd/)

- [RSI indicator](https://breakingdownfinance.com/trading-strategies/technical-analysis/rsi-indicator/)

- [Williams %R](https://breakingdownfinance.com/trading-strategies/technical-analysis/williams-r/)

- [Bollinger Bands](https://breakingdownfinance.com/trading-strategies/technical-analysis/bollinger-bands/)

- [Option strategies](https://breakingdownfinance.com/trading-strategies/option-strategies/)

- [Break-even Price Analysis](https://breakingdownfinance.com/finance-topics/derivative-valuation/option-valuation/break-even-price-analysis/)

- [Call Option Strategy](https://breakingdownfinance.com/trading-strategies/option-strategies/call-option-strategy/)

- [Covered call](https://breakingdownfinance.com/trading-strategies/option-strategies/covered-call/)

- [Naked Put Option Writing](https://breakingdownfinance.com/trading-strategies/option-strategies/naked-put-option-writing/)

- [Straddle](https://breakingdownfinance.com/trading-strategies/option-strategies/straddle/)

- [Contact us](https://breakingdownfinance.com/contact-us/)

- [**Menu** Menu](https://breakingdownfinance.com/finance-topics/risk-management/realized-volatility/)

[Home](https://breakingdownfinance.com/ "Breaking Down Finance")1 / [Finance topics](https://breakingdownfinance.com/finance-topics/ "Finance topics")2 / [Risk management](https://breakingdownfinance.com/finance-topics/risk-management/ "Risk management")3 / Realized Volatility

# Realized volatility

The realized volatility is a new rising concept in the financial literature. It is derived from the realized variance and introduced by Bandorff-Nielssen and Sheppard. It is often used to measure the price variability of intraday returns. Although it can also be used at lower data frequencies.

## Realized volatility formula

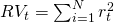

In order to calculate it, you first need to calculate the log returns of the security as shown in the formula below.

In a next step, the realized volatility is calculated by taking the sum over the past **N** squared return.

The realized volatility is simply the square root of the realized variance.

## Annualizing realized volatility

When having calculated the realized variance of a single day, this can be annualized in the following way. By calculating the realized variance of a single day using high frequency data, the annualized realized variance equals the daily realized variance multiplied by the amount of trading days.

The annualized realized volatility is simply the square root of the realized variance.

## Summary

The realized volatility, or in general the realized variance, is a new financial volatility concept unknown to many investors. It is a popular technical to measure intraday price risk. As such it is useful to extend standard risk management practices with this approach.

### Return calculation

Want to have an implementation in Excel? Download the Excel file: [realized volatility](https://breakingdownfinance.com/wp-content/uploads/2016/07/realized-volatility.xlsx)

### Pages

- [Home](https://breakingdownfinance.com/)

- [Alternative investments](https://breakingdownfinance.com/finance-topics/alternative-investments/)

- [Behavioural Finance](https://breakingdownfinance.com/finance-topics/behavioural-finance/)

- [Equity valuation](https://breakingdownfinance.com/finance-topics/equity-valuation/)

- [Finance basics](https://breakingdownfinance.com/finance-topics/finance-basics/)

Copyright - Breaking Down Finance

- [Terms of use](https://breakingdownfinance.com/disclaimer/)

- [Privacy Policy](https://breakingdownfinance.com/privacy-policy/)

- [Disclaimer](https://breakingdownfinance.com/disclaimer-2/)

[Scroll to top Scroll to top](https://breakingdownfinance.com/finance-topics/risk-management/realized-volatility/#top "Scroll to top")

You cannot copy content of this page |

| Readable Markdown | The realized volatility is a new rising concept in the financial literature. It is derived from the realized variance and introduced by Bandorff-Nielssen and Sheppard. It is often used to measure the price variability of intraday returns. Although it can also be used at lower data frequencies.

## Realized volatility formula

In order to calculate it, you first need to calculate the log returns of the security as shown in the formula below.

In a next step, the realized volatility is calculated by taking the sum over the past **N** squared return.

The realized volatility is simply the square root of the realized variance.

## Annualizing realized volatility

When having calculated the realized variance of a single day, this can be annualized in the following way. By calculating the realized variance of a single day using high frequency data, the annualized realized variance equals the daily realized variance multiplied by the amount of trading days.

The annualized realized volatility is simply the square root of the realized variance.

## Summary

The realized volatility, or in general the realized variance, is a new financial volatility concept unknown to many investors. It is a popular technical to measure intraday price risk. As such it is useful to extend standard risk management practices with this approach. |

| ML Classification | |

| ML Categories | null |

| ML Page Types | null |

| ML Intent Types | null |

| Content Metadata | |

| Language | en-us |

| Author | null |

| Publish Time | 2021-08-22 18:29:28 (4 years ago) |

| Original Publish Time | 2018-09-28 21:23:16 (7 years ago) |

| Republished | Yes |

| Word Count (Total) | 511 |

| Word Count (Content) | 210 |

| Links | |

| External Links | 0 |

| Internal Links | 102 |

| Technical SEO | |

| Meta Nofollow | No |

| Meta Noarchive | No |

| JS Rendered | No |

| Redirect Target | null |

| Performance | |

| Download Time (ms) | 483 |

| TTFB (ms) | 474 |

| Download Size (bytes) | 52,487 |

| Shard | 71 (laksa) |

| Root Hash | 13156206839566398671 |

| Unparsed URL | com,breakingdownfinance!/finance-topics/risk-management/realized-volatility/ s443 |